Trying to induce inflation to reduce accumulated debt is not a modern invention. Dr. Carmen Reinhart and Dr. Kenneth Rogoff trace this kind of financial crisis and others back to the Dionysius of Syracuse during the 4th century. The debasement of currency also occurred in the Roman empire and Byzantine empire and as usual printing money or devaluing your own currency does not usually lead to beneficial outcomes if we are to use history as any guide. We need to be upfront about what is going on here and that is the globe is reaching a peak debt situation. Think of the recent problems we have seen in Iceland, Ireland, and Greece. Yet these are simply tips of the visible iceberg of financial mania in our current system. Europe has many issues to contend with especially when looking at Spain, Italy, and Portugal. Here in the U.S. the Federal Reserve and U.S. Treasury are doing everything they can to ignore the reality of our current situation. Politicians are unable to make the hard choices and bankers simply want to extract productivity from the working classes. Our current predicament is not unusual in the books of history but the size and global interconnectedness is.

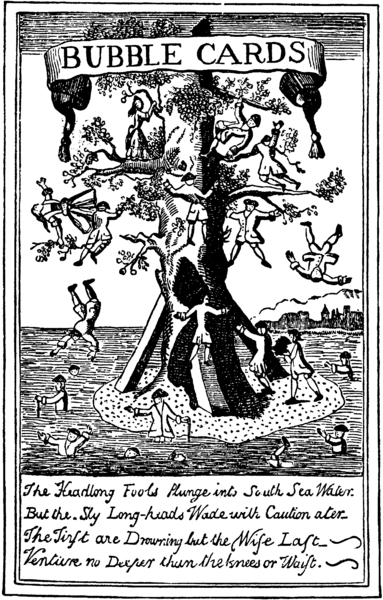

A history of manias and speculation south sea bubble

Source: Extraordinary Popular Delusions and the Madness of Crowds; Charles Mackay 1841/1852

Speculation is inherent in most financial panics. The above picture is from the South Sea Bubble of 1720 where investors speculated in South America. This was largely concentrated in the United Kingdom but had a parallel event with the Mississippi Bubble that concentrated speculation in France. Bubbles seem to spread so it is no surprise that Europe was whipped up in frenzy and when the bubble popped, the economies crashed and many were left in financial ruin. In both cases investments were exaggerated in value and many people got sucked into the desire for a quick buck. Banks like the Banque Générale Privée were more than happy to allow the speculation to continue. We can find many parallels in our banking system and how it was central to the U.S. real estate bubble.

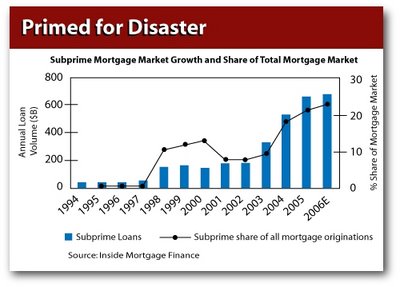

Let us rewind and look at the massive viral like expansion of subprime debt for example:

subprime Source: Inside Mortgage Finance

How is it possible that with historically low 30 year fixed mortgage rates that subprime loans were pushed onto the general public? As we now painfully know, many of these loans were aggressively pushed by mortgage brokers with the nudging of Wall Street to mostly poor working class Americans when either a more suitable 30 year conventional mortgage would have sufficed or frankly no mortgage at all because low income or no savings were even present as a buffer. Yet bubbles bring out the charlatans in every society. It is no slight irony that John Law, the Scottish economist was also a gambler and had the amazing ability to compute complex mathematical equations all in his head. He was also at the heart of the Mississippi Bubble that imploded wonderfully. Unlike a system of calculus or physics we find that economics tends to bend to the will of those in power. Wall Street hires economists that tend to favor their best outcomes even if bias is strewn all through the data. The fact that we are now living in the deepest economic crisis should tell us something about the power of the financial system we now have in place.

Imploding the financial system

Economic crisis and bubbles seem to happen all the time if we look close enough:

-1637: Tulip Mania (Netherlands)

-1720: South Sea and Mississippi (Great Britain and France)

-1792: Panic

-1813: Danish state bankruptcy declared

-1837: Deep US economic recession with bank failures followed by a 5 year depression

-1873: Known as Long Depression; 5 year depression

And more recently:

-1990: Japanese asset and stock market bubbles

-1994: Mexico economic crisis

-1997: Asian financial crisis

-2001: Bursting of dot-com bubble

-2007/present: bursting of real estate bubble and global debt bubble

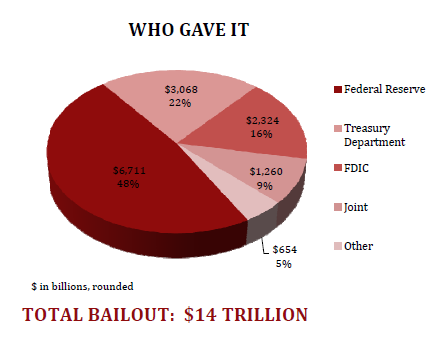

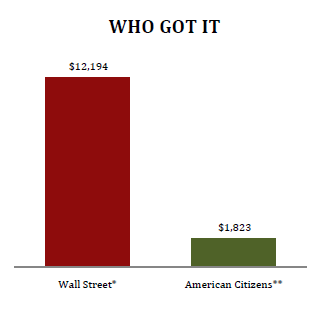

What can we learn from the above? We have yet to find a system that has rubbed out major financial panics. It is embedded in our current financial engineering for these things to occur. The issue of course is when these panics hit do we tweak the system to improve it or do we simply reinforce the underlying foundation to make things worse? In this crisis we have merely handed over trillions of dollars to the principal architects of the crisis with no reforms or dramatic changes to our system. The data is rather compelling:

total-bailout Source: It Takes a Pillage who-got-the-bailouts

I wonder how history will remember this financial crisis ten years from now. If things remain the same, historians will wonder how a society allowed a financial industry to simply raid their savings accounts and steal their productivity and then have the gall to request a taxpayer bailout for a mess they largely created. In a free market system (which we do not have contrary to banking mythology) the higher the risk you take, the more reward you can garner. Fail, and you can lose and even lose it all. The American public has lost a large amount in this crisis. Many have now lost the prospect of being able to afford for a good college education without going into debt servitude or having reasonably priced healthcare. Many have lost accessible industries that would provide a middle class lifestyle like that enjoyed from the previous generation. Many have paid dearly by losing their homes through foreclosure, seeing their savings dwindle to nothing, and facing rising costs even though we are told that inflation is controlled. Banks on the other hand have paid very little for this crisis and in fact the too big to fail have become even bigger and more powerful. Instead of failing as necessary they deemed it sufficient to use their political connections to maneuver massive bailouts that simply transferred wealth from the bottom right up to the top.

Charles Kindleberger sums it up best when he states:

Asset price bubbles in major industrial countries are rare; the previous bubble in the United States had been in the late 1920s. Japan had never had an asset price bubble before and neither had the Asian countries. A bubble in six or eight countries at the same time is an extraordinary phenomenon; nothing like it had ever happened before. But then four distinct asset price bubbles in a fifteen-year period was also unprecedented.

The above was written in 2005 from an expert on manias and panics. How many countries had asset bubbles this time? Let us see if we can beat four asset bubbles at once with this crisis:

Real estate bubbles in:

-United States (popped)

-Spain (popped)

-Ireland (popped)

-Britain (popping)

-Australia (popping)

-Canada (peaked will pop)

-China (peaking will pop)

Looks like we are going to rewrite the history on major panics with this financial crisis but let us hope we can learn lessons that develop a stronger system in place instead of allowing a systematic looting of financial wealth from the population.

Who died and left Standard & Poor'sa single, private company that specializes in credit rating and financial researchin charge of the nation's economy and its politics?

Last week, S&P decided that Congress mightjust mightget into another political dustup sometime in the future over an artificial, congressionally mandated line in the budget sand called the debt ceiling.

Apparently, the company preferred a target of $4 trillion in future budget cuts over the smaller cuts finally included in the most recent congressional deal to raise the debt ceiling.

Then, it issued a downgrade of the credit worthiness of the United States, tipping off a panic that has roiled the stock market all week long.

It is inexplicable why anyone would listen to S&P.

In its financial analysis of the impact of U.S. deficits, its analysts made a $2 trillion arithmetic error. Then, they admitted that their downgrade was based entirely on American politics and not on that financial analysis.

It isn't like S&P has a great record judging the financial health of national economies. Countries in real financial trouble now were the darlings of S&P not long ago. High finance gems like credit default swaps were rated AAA, right up to the time those gems collapsed. If individual investors had followed the advice of this company during the last five years, they would indeed be poor.

So what are we to do with the craziness S&P helped generate? Go outside, take a deep breath and ignore the blather. American companies are fine, and the market will recover, if we all stop listening to the likes of S&P.

Add Michael Moore to the list of critics railing against Standard & Poors cut to Americas credit rating.

Only the fiery social commentator and film director takes it one step further: He wants the head of S&P arrested.

On his Twitter feed Monday, Moore wrote:

Pres Obama, show some guts & arrest the CEO of Standard & Poors. These criminals brought down the economy in 2008& now they will do it again.

The 2008 reference is apparently because S&P and other rating agencies did not downgrade mortgage-based bonds, which encouraged the housing bubble behind the subprime crisis, says the Washington Times.

Owners of S&P are old Bush family friends, Moore writes in another Tweet, touching on a theme he developed in several movies slamming capitalism for being a old boys club for the rich and Wall Street.

Moore may have started something.

Tuesday morning, Business Insider reports, a plane flew by the S&P offices in New York dragging a banner behind it saying:

THANKS FOR THE DOWNGRADE. YOU SHOULD ALL BE FIRED.

This from Fortune on the identity of the critic:

[The woman who sent the plane is a] Midwestern investment banker broker who woke up last night with the need to vent at those who she believes are leading the nation into an economic morass.

I originally wanted to fly it over Washington, D.C., but learned that you cant do that, says the banker, who asked to remain anonymous for job security reasons [but later told The Daily her name]. So I chose Wall Street instead, but didnt specifically intend it to fly over S&P. Im just a mother from St. Louis who feels the only reason we got downgraded was people in politics.

Here are a few other prominent critics of the S&P downgrade:

Investing legend Warren Buffett: The S&P decision doesnt make sense.

I dont get it. In Omaha, the U.S. is still triple A. In fact, if there were a quadruple-A rating, Id give the U.S. that.

Treasury Secretary Timothy Geithner: Terrible judgement and a stunning lack of knowledge.

Legg Mason Inc.s Bill Miller: precipitous, wrong and dangerous.

President Barack Obama: No matter what some agency may say, we have always been and always will be a triple-A country.

On the thumbs-up side is Pimcos Bill Gross. The manager of the worlds biggest bond fund said S&P showed some spine and finally got it right.

Know of any other interesting reactions to S&Ps world-shaking downgrade. Let us know below in comments.

Re:We're Fucked - The Coming Economic Crisis

« Reply #169 on: 2011-11-08 17:22:02 »

I find it interesting, if not disturbing that these stories don't mention the elephant in the room; some very greedy people screwed the world.

Cheers

Fritz

Crushed economic recovery: Keynes and I did tell you so

Source: The Guardian Author: David Blanchflower Date: 2011.11.08

In 1930, John Maynard Keynes predicted 'the long, dragging conditions of semi-slump which may be expected to succeed the acute phase [of recession]'. Photograph: Tim Gidal/Getty Images

Cut spending in a recession, insist on austerity and what do you get?

In a Guardian op-ed on 14 July 2009, I warned:

"If you want to transform a recession into a depression, go ahead and cut public spending. I would advise against it and so, I believe, would John Maynard Keynes."

Not that it gives me any pleasure to say so, but that warning seems rather prescient right now, as did the famous quote from Keynes, written in 1930, just after the Great Crash but before the Great Depression, which I used to open the column.

"For it is a possibility that the duration of the slump may be much more prolonged than most people are expecting and much will be changed both in our ideas and in our methods before we emerge. Not, of course, the duration of the acute phase of the slump, but that of the long, dragging conditions of semi-slump, or at least sub-normal prosperity, which may be expected to succeed the acute phase."

A Guardian editorial on 10 September 2009 also cautioned about what would happen if stimulus was reversed too soon:

"Politicians must remember that a semi-slump will be almost as painful as the real thing. If the government Labour or Tory cut back now, they will crush a fragile recovery. The economy is unlikely to return to normal for a long time; neither should economic policy."

Unfortunately, policymakers did not heed these warnings and the strong growth that was generated by global action on both the fiscal and monetary fronts has now been tipped into reverse. Growth has gone south. Leaders failed to learn from the lessons of the US in 1937 when policy was tightened too soon, which then plunged the economy into a double-dip recession. It's a classic example of the old adage that if you don't learn from the lessons of history, you are doomed to repeat them.

Consumer and business confidence around the world is falling, real incomes are stagnating or even falling and unemployment remains unacceptably high across the OECD countries. Indeed, both in France and in the UK, unemployment has started to rise again, and both countries appear to be headed back into recession. The French government this week announced new austerity measures that are likely to compromise growth, just as they have in the UK. Italy continues to struggle to pass its austerity measures as bond yields spike as growth slows.

Last week, the Federal Open Market Committee (FOMC) lowered its forecasts for growth in the United States, and in recognition of the slowing, the three hawks moved away from tightening and there was even a lone dissenter, Charles Evans, president of the Chicago Fed, who wanted further easing. The latest labor market release from the BLS showed that employment grew by 80,000, but faster job creation than that is needed to get the unemployment rate down to more acceptable levels.

However, large cuts in public spending are on the way, as the super committee considers which areas of federal spending are to be slashed, while Obama's jobs package is on hold in Congress. That will reduce growth and raise unemployment, and this seems likely to push the Fed into doing a further burst of quantitative easing or QE3.

At the beginning of October, the Bank of England's MPC voted unanimously for more QE, in a move that few in the markets had expected, because of fears that the spreading crisis, which, it said in its statement, threatened the UK recovery. Employment over the last rolling three-month period fell by 178,000, and youth unemployment stands close to 1 million.

It now appears that the current recession is as deep but longer-lasting there than the 1930-34 double-dip recession, which had restored the level of output within four years, whereas in the current slump, under a half of the drop has been recovered after 44 months. The independent forecasting group NIESR now predicts that the UK would only achieve growth of 0.8% in 2011 and 0.9% in 2012, well below official forecasts, so it may well take several more years to get back to the level of output at the start of the recession. GDP growth over the last year has only been 0.5% and the November UK PMIs for manufacturing, construction and services suggest that growth in October was negative. There is every prospect, then, that fourth quarter 2011 and first quarter 2012 will both be negative and hence consistent with a technical recession. The UK coalition government seems to have no idea what to do.

Even though we have now moved from the acute phase of the Great Recession, which occurred in the fall of 2008, the long, dragging conditions of semi-slump and sub-normal prosperity have arrived and they aren't going away any time soon, as Keynes warned. The whole idea of an expansionary fiscal contraction was always fanciful in the extreme; now, it's time for a change of course given that austerity has failed. Growth is going to be low for many years, living standards are not going to rise, and the high levels of income inequality are all likely to contribute to increasing levels of social unrest. Much, indeed, will need to be changed.

Richard Duncan, formerly of the World Bank and chief economist at Blackhorse Asset Mgmt., says America's $16 trillion federal debt has escalated into a "death spiral, "as he told CNBC.

And it could result in a depression so severe that he doesn't "think our civilization could survive it."

And Duncan is not alone in warning that the U.S. economy may go into a "death spiral."

Since the recession, noted economists including Laurence Kotlikoff, a former member of President Reagan's Council of Economic Advisers, have come to similar conclusions.

Kotlikoff estimates the true fiscal gap is $211 trillion when unfunded entitlements like Social Security and Medicare are included.

However, while the debt crisis numbers are well known to most Americans, the economy hasn't suffered a major correction for almost 4 years.

So the questions remain: Is the threat of collapse for real? And if so, when?

A team of scientists, economists, and geopolitical analysts believes they have proof that the threat is indeed real - and the danger imminent.

One member of this team, Chris Martenson, a pathologist and former VP of a Fortune 300 company, explains their findings:

"We found an identical pattern in our debt, total credit market, and money supply that guarantees they're going to fail. This pattern is nearly the same as in any pyramid scheme, one that escalates exponentially fast before it collapses. Governments around the globe are chiefly responsible.

"And what's really disturbing about these findings is that the pattern isn't limited to our economy. We found the same catastrophic pattern in our energy, food, and water systems as well."

According to Martenson: "These systems could all implode at the same time. Food, water, energy, money. Everything."

Another member of this team, Keith Fitz-Gerald, the president of The Fitz-Gerald Group, went on to explain their discoveries.

"What this pattern represents is a dangerous countdown clock that's quickly approaching zero. And when it does, the resulting chaos is going to crush Americans," Fitz-Gerald says.

Dr. Kent Moors, an adviser to 16 world governments on energy issues as well as a member of two U.S. State Department task forces on energy also voiced concerns over what he and his colleagues uncovered.

"Most frightening of all is how this exact same pattern keeps appearing in virtually every system critical to our society and way of life," Dr. Moors stated.

"It's a pattern that's hard to see unless you understand the way a catastrophe like this gains traction," Dr. Moors says. "At first, it's almost impossible to perceive. Everything looks fine, just like in every pyramid scheme. Yet the insidious growth of the virus keeps doubling in size, over and over again - in shorter and shorter periods of time - until it hits unsustainable levels. And it collapses the system."

Martenson points to the U.S. total credit market debt as an example of this unnerving pattern.

"For 30 years - from the 1940s through the 1970s - our total credit market debt was moderate and entirely reasonable," he says. "But then in seven years, from 1970 to 1977, it quickly doubled. And then it doubled again in seven more years. Then five years to double a third time. And then it doubled two more times after that.

"Where we were sitting at a total credit market debt that was 158% larger than our GDP in the early 1940s... By 2011 that figure was 357%."

Dr. Moors warns this type of unsustainable road to collapse can be seen today in our energy, food and water production. All are tightly connected and contributing to the economic disaster that lies directly ahead. Keith Fiz-Gerald: Germany's military held a secret investigation into this unsustainable pattern and concluded it could lead to "political instability and extremism." Details here

According to polls, the average American is sensing danger. A recent survey found that 61% of Americans believe a catastrophe is looming - yet only 15% feel prepared for such a deeply troubling event.

Fitz-Gerald says people should take steps to protect themselves from what is happening. "The amount of risky financial derivatives floating around the globe is as much as 20 times size of the entire GDP of the world," he says. "It's unsustainable and impossible to unwind in any kind of orderly way."

Moreover, he adds: "People can also forget that the FDIC can only cover a fraction of US bank deposits. It's a false sense of security. Just like state pensions, which could be suspended at any time. A collapse could wipe out these programs. Entitlements like Social Security and Medicare are already bankrupt and simply being propped up."

We can see the strain on society already.

In two years, Congress won't have any money for transportation, reports the Washington Post. Cities like Trenton, NJ have layed off one-third of their police force due to budget cuts. And other cities like Colorado Springs, CO removed one-third of streetlights, trashcans, and bus routes, reports CNN.

Fitz-Gerald also warns of a period of devastating inflation. A recent survey, reports USA Today, notes that in the coming years it could take $150,000 a year in household income for a family to afford basic living expenses - and maybe go out to a movie.

Right now, in fact, "52% of Americans feel they barely have enough to afford the basics."

"If our research is right," says Fitz-Gerald, "Americans will have to make some tough choices on how they'll go about surviving when basic necessities become nearly unaffordable and the economy becomes dangerously unstable."

"People need to begin to make preparations with their investments, retirement savings, and personal finances before it's too late," says Fitz-Gerald.

Re:We're Fucked - The Coming Economic Crisis

« Reply #172 on: 2012-12-19 10:26:45 »

Since the tainted British banking system is what the America system is model on and cross pollinated with, I'm thinking it would be safe to say ours is tainted as well. To yearn for the days of gangsters and crime lords when it was obvious who the good guys and bad guys were.

Cheers

Fritz

Another Goldman Creature Given Vital Government Post

Governor of the Bank of Canada Mark Carney speaks during a press conference in Mexico City. YURI CORTEZ/AFP/Getty Images

Big news yesterday in the United Kingdom, where the citizenry surveyed its domestic banking system and discovered that it couldn't find a single person trustworthy enough to put in the top job at the Bank of England. So they went to Canada and stole that country's central banker, Mark Carney, who just happens to be a former Goldman, Sachs executive he was once Goldman's managing director of investment banking.

Carney's appointment may be seen as an admission that the British banking sector is now so tainted, only an outsider can be trusted to govern them. Almost all of the major English banks have been dinged by ugly scandals. The LIBOR mess, in which banks have been caught messing around with global interest rates for a variety of sordid reasons, has most infamously implicated Barclays, but the Royal Bank of Scotland is also a cooperator in those investigations.

Meanwhile, HSBC has been accused of laundering billions of dollars of Mexican drug money, a monstrous mess that recalls the infamous Bank of New York scandal of the late Nineties involving Russian mob money; officials have described the HSBC culture as "pervasively polluted." And the British bank Standard Chartered is now being forced to pay $330 million to settle claims that it laundered hundreds of billions of dollars on behalf of Iran.

But Mark Carney is no Elliott Ness, brought in from the outside to clean the streets of Chicago. Instead, he's another Geithner-esque character who will almost certainly prefer a hands-off regulatory approach, and seems to view the power of the government and the central bank as being necessary mainly to help bolster public confidence in the banking system. He'll likely be another central banker in the mold of Ben Bernanke, who's used endless rivers of cheap loans and money-printing programs like Quantitative Easing to keep floating corrupt banks all night long, for as long as they want to keep playing the roulette table. Here's the Guardian's prediction with regard to Carney:

He and many others in central bank circles know that most of the Britain's banks are very highly leveraged. That without the support of the Bank of England's quantitative easing programme, and its very low lending rates all effectively backed by British taxpayers Britain's banks would effectively be insolvent.

And so Carney will continue with quantitative easing which has provided British banks with the liquidity needed to indulge in speculative activity both at home and abroad, speculative activity that bears a scary resemblance to that undertaken before the crisis.

What the banking system really needs is a guy who will step in and force bankers to go back to being boring, risk-averse drips who lend businesses money to buy new equipment or fleets of trucks or whatever. What we have instead are coked-up wannabe big shots straight out of Boiler Room who are washing Mexican drug money and laundering Middle Eastern cash and playing around with wild price-fixing schemes pretty much everything you can think of that isn't quietly counting beans and helping grow the economy.

The British have a tough job ahead trying to clean that mess up, but appointing another Goldman vet to a crucial government job the latest in a long line of such appointments, stretching from Bob Rubin to Hank Paulson to Neel Kashkari to former Ex-Im Bank chief Kenneth Brody, former Bush chief of staff Josh Bolten, and former Fannie Mae president James Johnson doesn't sound like a good start.

When I was last in France, I came across a manuscript hidden behind a panel in one of the quieter wings of the Louvre palace. (I try to vandalise a major monument whenever I visit in Paris.)

It turned out the single, closely-written sheet was apparently a previously unknown work by Voltaire, who if I remember right was the guy who invented electricity. So the discovery might be interesting for some.

Between my schoolboy French and Google Translate I managed to knock out an English version before customs confiscated the original under some stupid international treaty.

***

Chapter 1 How A Young Man Was Brought Up in a Magnificent Castle and How He Was Driven Thence

In the castle of the most noble Baron of Planetki, lived a Youth whom nature had endowed with a most amiable disposition. The old servants of the house suspected him to have been the production of a forbidden liaison between the Barons sister (a too-passionate conservative) and a liberal member of the local gentry who (the door and the window being secured) had, so the story went, got into her bedroom using the third way.

The Tutor to the children of the castle taught neo-incrimental-postideological-frogboiling-conservatism, and could demonstrate by assertion that Planetki was the best-governed of all possible estates and the Barons polices the most sensible of all possible policies (all of which were likely to achieve their claimed intention). For these skills he had been granted residency by the Baron, which was clearly an honour even if nobody quite knew what it meant.

The Tutor was the oracle of the family. The Youth in particular absorbed his precepts with all the simplicity natural to his age and disposition. The lessons were not onerous, for though the Tutor assigned a great many text books, he did not require his students to read them as long as they claimed they had read a newspaper article on the subject.

Are we not all happy? the Tutor said as he stood before his students on one of the estates many golf courses (and the Youth could not deny that he was happy, sitting next to the comely daughter of the Baron), Observe, for instance,how everything here is conducive to growth. Though this potplant (here he brandished that item) may appear barren, its underlying conditions (indicating the presumptive roots) are sound. When Spring comes (the season was late Winter and had been for some time) it will blossom forth with unparalleled verdancy. And when it does so, all our practises will enhance its development.

Do we not, rather than using so-called toilets, relieve ourselves where-ever we are inclined? This enhances the fertility of our environment, contributing to the greenness for which Planetkis land and rivers are justly famous. So you see, everything is arranged to maximise growth.

Some time earlier the Tutor had demonstrated this by an experiment called growing the pie. The Youth had been duly impressed when, some weeks later, the pie in question was indeed larger everyones share having increased in volume by the addition of a quantity of soft grey fuzz which the Youth took to have materialised through the principle of self-sufficiency.

But on this occasion the Barons son indelicately suggested the potplant might indeed be dead, and furthermore that it looked quite like it was just a stick poked in some dirt. (The Barons son had a somewhat oppositional nature.) Oh no it isnt, the Tutor replied. The Youth was looking forward to seeing his preceptor rebut the objection point by point, but it happened that at that moment a beggar approached.

The master had inculcated in his students that to go about being poor, in such a well-governed and prosperous realm as Planetki, was a personal failing that demonstrated at the least ingratitude and at the worst criminality. So they had agreed between them to enforce a social contract under which anybody asking for food or shelter had rocks thrown at them. This was considered a win/win as it also provided the students with regular healthy exercise. In deference to objections from the Barons son who accepted the need to incentivise non-begging but was concerned about extreme methods the Tutor insisted they should try not to cause any permanent injury.

Now, about that potplant said the Barons son once the excited students settled down.

What potplant? inquired the Tutor blithely (having earlier hurled it at the back of the fleeing beggar). He had an excellent memory for catchphrases but once he had forgotten an inconvenient fact he could not be persuaded to remember it. So they were obliged to resume their lessons on another topic.

Following the afternoons lesson the Youth walked with the Barons daughter to a secluded sand trap. There he declared his ambition (though he was a little vague one the details) for efficent delivery of a win/win outcome regarding her aspirational targets. The young lady for her part was open to innovative ideas, and the young couple were soon concealed against the sandy bank investigating ways to rebalance their opportunities.

The Youth was investigating the effect direct stimulus of his ladys underlying conditions had on her wider economy (and she was drawing increasingly positive growth projections from his external influences) when a passing greenkeeper noted their compromising fiscal position. Realising there was an imminent risk of unrestrained quantitative easing, he raised the alarm.

The Baron arrived and by way of penalty first administered a sound kick to the Youths economic fundamentals then declared he would be exiled. The Youth desperately tried to explain about the tight fiscal conditions and the public/private delivery models of vital services. On hearing this, the Baron also expelled the Tutor as a bad influence, and would have charged them both with a crime if he could.

(Under Planetkis criminal law, if the supreme court finds you were breaking the law you actually werent; if a statute of limitations had expired it was never illegal; if the police do not charge you no law was broken (except when it was); and as long as an inspector-general inquires into your actions and your minister expresses disappointment, you can get away with anything. The Tutor had once described this as an ideal balance of justice and efficiency. Planetki has no courts.)

As they fled, the Youth realised they might now be considered unemployed, and offered to protect his master from flying rocks. But the Tutor explained that they were in fact between contracts, or merely observing one of those many holidays enjoyed by the citizens of Planetki (especially those who work in manufacturing).

The roads in that region were well-paved and entirely empty so they made fast progress. Soon they had left Planetki entirely (or at least, arrived at that part of Planetki that had been sold to pay for the roads).

And so they went into the world, the Tutor commiserating with the distraught Youth over his troubles, and agreeing that it was all the fault of those damnable external influences, which one cannot be expected to control.

***

Which I guess would be just the start of their adventures, but here the body of the manuscript ends.

There are notes towards more. For example: a ship the pair are travelling in sinks in a storm. On the Tutors advice they stay afloat by clinging to a sinking coalition partner.

They land shortly before a devastating earthquake. The Tutor sees this as an excellent chance to propose various neo-incrimental-postideological-frogboiling-conservative methods that might otherwise have been unacceptable; a plan which is only arrested when the local citizens have the good sense to burn him at the stake.

Also just a note about unruly natives.

But it looks like at this point the author just gave up on the project, having decided the political philosophy in question was too obviously stupid and incoherent to justify a whole book.

Re:We're Fucked - The Coming Economic Crisis

« Reply #174 on: 2013-03-31 21:48:14 »

[Fritz]A case in point. And they have payed back the IMF loan. Court cases from Europe from inventors in the failed Icelandic banks are still on going. To big to Fail = Welfare for the Bankers ... it would seem.

Re:We're Fucked - The Coming Economic Crisis

« Reply #175 on: 2013-04-09 10:49:58 »

The BRICS kids on the block are mussling in on the existing world order; and the homies aren't gett'in down wid it. Or "Rumble in the Banks" ... or is BITCoin the real winner ? ... clearing the $200.00 mark today.

Cheers

Fritz

Brics bank raises critical development questions, says OECD

Source: The Guardian Author: Mark Tran Date: 2013.04.09

OECD's Angel Garría says devil is in detail market rates, policy demands and how loans will be made of any new Brics bank

South Africa's Pravin Gordhan and Jacob Zuma at the Brics summit in Durban, which agreed in principle to set up a new bank. Photograph: Rogan Ward/Reuters

The creation of a development bank by the five big emerging economies of Brazil, Russia, India, China and South Africa, known as the Brics, is welcome but raises critical questions, according to the head of the Organisation for Economic Co-operation and Development (OECD).

Angel Garría, secretary general of the OECD, said an important consideration will be the new bank's criteria for loans, or conditionality.

"Will it lend at market rates and what policy conditionality will be attached to the loans?" he said in an interview with the Guardian. "What we know about development banking is that the loan itself is the least important aspect; it's the policy related to the loan the policy conditionality. Or will the loans be like IDA [International Development Association] loans?"

The World Bank's soft loan arm, the IDA lends money on easy terms, charging little or no interest. Repayments are stretched over 25 to 40 years, including a five- to 10-year grace period. The IDA also provides grants to countries at risk of debt distress.

The IDA is one of the largest sources of assistance for the world's 81 poorest countries, 39 of them in Africa, and is the single largest source of donor funds for basic social services in these countries.

The Brics have in principle agreed to create a development bank to provide initial funding for infrastructure projects worth $4.5tn (£3tn).

Plans were announced last month in Durban, South Africa, where the Brics declared that the bank represented part of a "new paradigm", reflecting a shift in economic power away from the west.

A Brics bank could provide an alternative to western-dominated financial institutions the International Monetary Fund (IMF), the World Bank, and regional development banks in Africa, Asia and Latin America that followed the second world war. Jim Yong Kim, the World Bank president, recently welcomed the prospect of a Brics development bank to help meet massive infrastructure needs in middle-income countries.

Developing countries have criticised the World Bank and the IMF for attaching neoliberal conditions to their loans, including privatisation of public services such as water and health, and premature liberalisation of markets.

The development bank would be the first institution of the informal Brics forum, which launched in 2009 amid the global financial crisis, representing 43% of the world's population and 17% of trade.

Pravin Gordhan, South Africa's finance minister, said in Durban plans were moving with "a great sense of urgency". Other developing countries would eventually be invited to join the bank, he said, adding that India had proposed $50bn of seed capital to get the initiative started, although no final decision had been reached.

Talk of a new development bank comes against a backdrop of falling official development assistance (ODA) from rich countries for the second successive year. In this context, Garría said the possibility of new financing additionality was welcome and a constructive declaration of south-south co-operation. The question was how the bank would work in practice.

The Durban agreement revealed little detail about the prospective bank: how much seed capital the bank will start with or where it will be headquartered.

Garría also wondered how it would fit into the development landscape. "What kind of niche or blind spot, what is the missing link are the Brics trying to fill?" asked Garria. "How will they apply this financing in practice? Today, there are more questions than answers. It's very welcome but like everything else the devil will be in the details."

Re:We're Fucked - The Coming Economic Crisis

« Reply #176 on: 2013-07-19 09:50:39 »

The Long Road to 'Recovery' .......

Cheers

Fritz

Source: The New York Times Author: MONICA DAVEY and MARY WILLIAMS WALSH Date: 2013.07.18

DETROIT Detroit, the cradle of Americas automobile industry and once the nations fourth-most-populous city, filed for bankruptcy on Thursday, the largest American city ever to take such a course.

The decision, confirmed by officials after it trickled out in late afternoon news reports, also amounts to the largest municipal bankruptcy filing in American history in terms of debt.

This is a difficult step, but the only viable option to address a problem that has been six decades in the making, said Gov. Rick Snyder, who authorized the move after a recommendation from the emergency financial manager he had appointed to resolve Detroits dire financial situation.

Not everyone agrees how much Detroit owes, but Kevyn D. Orr, the emergency manager, has said the debt is likely to be $18 billion and perhaps as much as $20 billion.

For Detroit, the filing came as a painful reminder of a citys rise and fall.

Its sad, but you could see the writing on the wall, said Terence Tyson, a city worker who learned of the bankruptcy as he left his job at Detroits municipal building on Thursday evening. Like many there, he seemed to react with muted resignation and uncertainty about what lies ahead, but not surprise. This has been coming for ages.

Detroit expanded at a stunning rate in the first half of the 20th century with the arrival of the automobile industry, and then shrank away in recent decades at a similarly remarkable pace. A city of 1.8 million in 1950, it is now home to 700,000 people, as well as to tens of thousands of abandoned buildings, vacant lots and unlit streets.

From here, there is no road map for Detroits recovery, not least of all because municipal bankruptcies are rare. State officials said ordinary city business would carry on as before, even as city leaders take their case to a judge, first to prove that the city is so financially troubled as to be eligible for bankruptcy, and later to argue that Detroits creditors and representatives of city workers and municipal retirees ought to settle for less than they once expected.

Some bankruptcy experts and city leaders bemoaned the likely fallout from the filing, including the stigma. They anticipate further benefit cuts for city workers and retirees, more reductions in services for residents, and a detrimental effect on borrowing.

For a struggling family I can see bankruptcy, but for a big city like this, can it really work? said Diane Robinson, an office assistant who has worked for the city for 20 years. What will happen to city retirees on fixed incomes?

But others, including some Detroit business leaders who have seen a rise in private investment downtown despite the citys larger struggles, said bankruptcy seemed the only choice left and one that might finally lead to a desperately needed overhaul of city services and to a plan to pay off some reduced version of the overwhelming debts. In short, a new start.

The worst thing we can do is ignore a problem, said Sandy K. Baruah, president of the Detroit Regional Chamber. Were finally executing a fix.

The decision to go to court signaled a breakdown after weeks of tense negotiations, in which Mr. Orr had been trying to persuade creditors to accept pennies on the dollar and unions to accept cuts in benefits.

All along, the states involvement including Mr. Snyders decision to send in an emergency manager has carried racial implications, setting off a wave of concerns for some in Detroit that the mostly white Republican-led state government was trying to seize control of Detroit, a Democratic city where more than 80 percent of residents are black.

The nature of Detroits situation ensures that it will be watched intensely by the municipal bond market, by public sector unions, and by leaders of other financially challenged cities around the country. Just over 60 cities, towns, villages and counties have filed under Chapter 9, the court proceeding used by municipalities, since the mid-1950s.

Leaders in Washington and in Lansing, the state capital, issued statements of concern late Thursday. A White House spokeswoman said President Obama and his senior team were closely monitoring the situation.

While leaders on the ground in Michigan and the citys creditors understand that they must find a solution to Detroits serious financial challenge, we remain committed to continuing our strong partnership with Detroit as it works to recover and revitalize and maintain its status as one of Americas great cities, Amy Brundage, the spokeswoman, said in a statement.

The debt in Detroit dwarfs that of Jefferson County, Ala., which had been the nations largest municipal bankruptcy, having filed in 2011 with about $4 billion in debt. The population of Detroit, the largest city in Michigan, is more than twice that of Stockton, Calif., which filed for bankruptcy in 2012 and had been the nations most populous city to do so.

Other major cities, including New York and Cleveland in the 1970s and Philadelphia two decades later, have teetered near the edge of financial ruin, but ultimately found solutions other than federal court. Detroits struggle, experts say, is particularly dire because it is not limited to a single event or one failed financial deal, like the troubled sewer system largely responsible for Jefferson Countys downfall.

Instead, numerous factors over many years have brought Detroit to this point, including a shrunken tax base but still a huge, 139-square-mile city to maintain; overwhelming health care and pension costs; repeated efforts to manage mounting debts with still more borrowing; annual deficits in the citys operating budget since 2008; and city services crippled by aged computer systems, poor record-keeping and widespread dysfunction.

All of that makes bankruptcy a process that could take months, if not years, and is itself expected to be costly particularly complex.

Its not enough to say, lets reduce debt, said James E. Spiotto, an expert in municipal bankruptcy at the law firm of Chapman and Cutler in Chicago. At the end of the day, you need a real recovery plan. Otherwise youre just going to repeat the whole thing over again.

The municipal bond market will be paying particular attention to Detroit because of what it may mean for investing in general obligation bonds. In recent weeks, as Detroit officials have proposed paying off small fractions of what the city owes, they have indicated they intend to treat investors holding general obligation bonds as having no higher priority for payment than, for instance, city workers a notion that conflicts with the conventions of the market, where general obligation bonds have been seen as among the safest investments and all but certain to be paid in full.

Leaders of public sector unions and municipal retirees around the nation will be focused on whether Detroit is permitted to slash pension benefits, despite a provision in the State Constitution that union leaders say bars such cuts.

Officials in other financially troubled cities may feel encouraged to follow Detroits path, some experts say. A rush of municipal bankruptcies appears unlikely, though, and leaders of other cities will want to see how this case turns out, particularly when it comes to pension and retiree health care costs, said Karol K. Denniston, a bankruptcy lawyer with Schiff Hardin who is advising a taxpayer group that came together in Stockton after its bankruptcy.

If you end up with precedent that allows the restructuring of retirement benefits in bankruptcy court, that will make it an attractive option for cities, Ms. Denniston said. Detroit is going to be a huge test kitchen.

Around this city, there was widespread uncertainty about what bankruptcy might really mean, now and in the long term. Officials said city workers were being sent letters, notifying them that city business would proceed as usual, from bills to permits. A hot line was planned for residents and others with questions and worries.

For some Detroiters, recent memories of bankruptcies by Chrysler and General Motors and the re-emergence of those companies appeared to have calmed nerves. But experts say corporate bankruptcy procedures are significantly different from municipal bankruptcies.

In municipal bankruptcies, for instance, the ability of judges to intervene in how a city is run is sharply limited. And municipal bankruptcies are a form of debt adjustment, as opposed to liquidation or reorganization.

Here, residents are likely to see little immediate change from the way the city has been run since March, when Mr. Orr arrived to oversee major decisions. A bankruptcy lawyer, he is widely expected to continue to run Detroit during a legal process. Mayor Dave Bing and Detroits elected City Council are still paid to hold office and are permitted to make decisions about day-to-day operations, though Mr. Orr could remove those powers.

Mr. Orr has said that as part of any restructuring he wants to spend about $1.25 billion on improving city infrastructure and services. But a major concern for Detroit residents remains the possibility that services, already severely lacking, might be further diminished in bankruptcy.

About 40 percent of the citys streetlights do not work, a report from Mr. Orrs office showed. More than half of Detroits parks have closed since 2008.

Monica Davey reported from Detroit, and Mary Williams Walsh from New York.

It is so sad to watch one of America's greatest cities die a horrible death. Once upon a time, the city of Detroit was a teeming metropolis of 1.8 million people and it had the highest per capita income in the United States. Now it is a rotting, decaying hellhole of about 700,000 people that the rest of the world makes jokes about. On Thursday, we learned that the decision had been made for the city of Detroit to formally file for Chapter 9 bankruptcy. It was going to be the largest municipal bankruptcy in the history of the United States by far, but on Friday it was stopped at least temporarily by an Ingham County judge.

She ruled that Detroit's bankruptcy filing violates the Michigan Constitution because it would result in reduced pension payments for retired workers. She also stated that Detroit's bankruptcy filing was "also not honoring the (United States) president, who took (Detroits auto companies) out of bankruptcy", and she ordered that a copy of her judgment be sent to Barack Obama. How "honoring the president" has anything to do with the bankruptcy of Detroit is a bit of a mystery, but what that judge has done is ensured that there will be months of legal wrangling ahead over Detroit's money woes.

It will be very interesting to see how all of this plays out. But one thing is for sure - the city of Detroit is flat broke. One of the greatest cities in the history of the world is just a shell of its former self. The following are 25 facts about the fall of Detroit that will leave you shaking your head...

1) At this point, the city of Detroit owes money to more than 100,000 creditors.

2) Detroit is facing $20 billion in debt and unfunded liabilities. That breaks down to more than $25,000 per resident.

3) Back in 1960, the city of Detroit actually had the highest per-capita income in the entire nation.

4) In 1950, there were about 296,000 manufacturing jobs in Detroit. Today, there are less than 27,000.

5) Between December 2000 and December 2010, 48 percent of the manufacturing jobs in the state of Michigan were lost.

6) There are lots of houses available for sale in Detroit right now for $500 or less.

7) At this point, there are approximately 78,000 abandoned homes in the city.

8 ) About one-third of Detroit's 140 square miles is either vacant or derelict.

9) An astounding 47 percent of the residents of the city of Detroit are functionally illiterate.

10) Less than half of the residents of Detroit over the age of 16 are working at this point.

11) If you can believe it, 60 percent of all children in the city of Detroit are living in poverty.

12) Detroit was once the fourth-largest city in the United States, but over the past 60 years the population of Detroit has fallen by 63 percent.

13) The city of Detroit is now very heavily dependent on the tax revenue it pulls in from the casinos in the city. Right now, Detroit is bringing in about 11 million dollars a month in tax revenue from the casinos.

14) There are 70 "Superfund" hazardous waste sites in Detroit.

15) 40 percent of the street lights do not work.

16) Only about a third of the ambulances are running.

17) Some ambulances in the city of Detroit have been used for so long that they have more than 250,000 miles on them.

18) Two-thirds of the parks in the city of Detroit have been permanently closed down since 2008.

19) The size of the police force in Detroit has been cut by about 40 percent over the past decade.

20) When you call the police in Detroit, it takes them an average of 58 minutes to respond.

21) Due to budget cutbacks, most police stations in Detroit are now closed to the public for 16 hours a day.

22) The violent crime rate in Detroit is five times higher than the national average.

23) The murder rate in Detroit is 11 times higher than it is in New York City.

24) Today, police solve less than 10 percent of the crimes that are committed in Detroit.

25) Crime has gotten so bad in Detroit that even the police are telling people to "enter Detroit at your own risk".

It is easy to point fingers and mock Detroit, but the truth is that the rest of America is going down the exact same path that Detroit has gone down.

Detroit just got there first.

All over this country, there are hundreds of state and local governments that are also on the verge of financial ruin...

"Everyone will say, 'Oh well, it's Detroit. I thought it was already in bankruptcy,' " said Michigan State University economist Eric Scorsone. "But Detroit is not unique. It's the same in Chicago and New York and San Diego and San Jose. It's a lot of major cities in this country. They may not be as extreme as Detroit, but a lot of them face the same problems."

A while back, Meredith Whitney was highly criticized for predicting that there would be a huge wave of municipal defaults in this country. When it didn't happen, the critics let her have it mercilessly.

But Meredith Whitney was not wrong.

She was just early.

Detroit is only just the beginning. When the next major financial crisis strikes, we are going to see a wave of municipal bankruptcies unlike anything we have ever seen before.

And of course the biggest debt problem of all in this country is the U.S. government. We are going to pay a great price for piling up nearly 17 trillion dollars of debt and over 200 trillion dollars of unfunded liabilities.

All over the nation, our economic infrastructure is being gutted, debt levels are exploding and poverty is spreading. We are consuming far more wealth than we are producing, and our share of global GDP has been declining dramatically.

We have been living way above our means for so long that we think it is "normal", but an extremely painful "adjustment" is coming and most Americans are not going to know how to handle it.

So don't laugh at Detroit. The economic pain that Detroit is experiencing will be coming to your area of the country soon enough

Re:We're Fucked - The Coming Economic Crisis

« Reply #178 on: 2013-08-06 10:14:16 »

Well now finally someone is talking about the elephant in the room: "The real reason that the US economy cannot recover is that it has been moved offshore"

Cheers

Fritz

Time is running out for the US economy and the American people

Time is running out for the US economy and the American people. The financial press and economic commentators, with few exceptions, do a good job of keeping this fact from the public.

Consider for example the spin put on the advance estimate of the real GDP growth rate for the second quarter announced on July 31. The annual rate of 1.7 percent real GDP growth for the second quarter of 2013 was presented optimistically as an acceleration in real GDP from the first quarters 1.1 percent growth rate. However, the reason for the acceleration in growth is that the first quarters estimate was revised down from 1.8 percent to 1.1 percent. The second quarter GDP growth rate is also subject to revised estimates. Most likely, the final number will be lower.

Consider also that the reason that real GDP is positive is that nominal GDP is deflated with an understated measure of inflation. The measure of inflation has been manipulated in order to deny Social Security recipients cost of living adjustments. Statistician John Williams (shadowstats.com) reports that if deflated by previous official methodology, GDP growth has been negative since the downturn in 2007. In other words, the recovery is just another government hoax.

Another failure of the financial press and economic commentators is the interpretation of the Federal Reserves policy of Quantitative Easing. The Fed is said to be keeping interest rates low in order to stimulate business investment and the housing market. This explanation is nothing but cover for the real purpose of QE, which is to drive up and keep high the debt related derivatives on the books of the banks too big too fail. Low interest rates pull up the prices of all debt instruments, and the higher prices raise the values on the banks balance sheets, making the banks look more solvent or less insolvent.

The Fed has continued QE for years, despite the policys failure to revive the economy, in order to hold the banks collapse at bay in the hopes that the banks would succeed in boosting their earnings sufficiently to get out of trouble.

The Feds QE policy has been costly for important areas of the economy. Retirees have

been denied interest income. This has reduced consumer expenditures and, thereby, GDP growth, and it has forced retirees to draw down their savings in order to pay their bills.

The Feds QE policy has also jeopardized the US dollar because of the several-fold increase in the number of dollars over the last few years. In order to support bond prices, the Fed has created 1,000 billion new dollars annually over the last several years. The supply of dollars has out grown the demand for dollars, putting the dollars exchange value under pressure. To protect the dollar from QE, the Fed and its dependent bullion banks have engaged in ruthless shorting of gold in order to suppress the price of gold. The rapidly rising gold price indicated falling confidence in the dollar, and the Fed feared that this lack of confidence would spread into the currency markets.

By printing dollars to support the banks, the Fed has created a bond market bubble, a stock market bubble, and a dollar bubble. If the Fed stops printing money, not only will the banks balance sheets take a hit, but so will the bond, stock, and real estate markets. Wealth would be wiped out. No one could any longer pretend that there is an economic recovery.

The impact on the dollar is less clear. On the one hand, curtailment of the dollars rapid increase in supply would help the currency. On the other hand, the drop in values of dollar-denominated assets, such as stocks, bonds, and real estate could cause the demand for dollars to decrease. Foreigners for example who sell dollar-based assets might also convert their dollar proceeds into their domestic currencies.

The failures of the financial press require the explanation that I have provided of QE, the bubble economy, and the manipulated measures of real GDP, inflation, and unemployment. However, although these explanations are necessary, they are themselves a diversion.

The real reason that the US economy cannot recover is that it has been moved offshore. Millions of US manufacturing and tradable professional service jobs such as software engineering have been moved to China, India and other countries where wages and salaries are a fraction of those in the US. Using free trade as a cloak, corporations have turned labor costs into a profits center. The drop in labor costs raises profits, which are then distributed to executives as performance bonuses and to shareholders as capital gains. The impact on US employment can be seen from the BLS monthly payroll jobs data and from the declining US labor force participation rate. The participation rate is not falling because consumer incomes are rising and fewer family members are needed in the work force. The rate is falling because discouraged workers have given up looking for employment and have left the work force.

The use of foreign labor in place of US labor is beneficial to executives and shareholders in the short-run, but it is detrimental in the longer-run. The long-run effect is to destroy the US consumer market.

When jobs offshoring halted the rise in US consumer income, in order to keep the economy going the Federal Reserve substituted a growth in consumer debt for the missing growth in consumer income. For example, the housing bubble created by Federal Reserve chairman Alan Greenspan allowed home owners to spend the inflated equity in their homes by refinancing their mortgages. The substitution of consumer debt for the missing growth in real wages and salaries is limited by the burden of debt on households. Unlike the government, American citizens cannot print the money with which to pay their bills. Once consumers were unable to take on more debt, the consumer economy ceased to expand.

The government can print money with which to pay its bills, but if history is a guide, governments cannot forever print money without serious consequences. The real economic crisis will hit when the bubble economy can no longer be supported by the printing press.

It should be obvious to economists, but apparently is not, that Walmart-type jobs of the New Economy do not pay sufficiently to support a consumer-dependent economy. As Obamacare is phased in, consumer purchasing power will suffer another blow. Even the subsidized premiums are expensive, and the cost of using the policies in terms of deductions and co-pays will be prohibitive for most. As employer-provided benefits and Medicare are cut back, the health care crisis will worsen in the midst of an economic crisis.

The scary part of the pending economic crisis occurs when the federal budget deficit widens as the economy contracts and the Fed finds itself in a situation where it cannot print yet more dollars without causing a loss in confidence in the dollar and US Treasury bonds. What does a desperate government do in such a situation? It confiscates what remains of private pensions, piles on taxes, and drives the people and the economy deeper into the ground.

This is the path that US economic policy is on. What is the solution?

Capitalism could be allowed to work and the banks to fail. It is cheaper to bail out depositors than to bail out the banks.

Corporations could be taxed on the basis of the geographical location at which value is added to their product. If corporations create the goods abroad that they market to Americans, they would have a high tax rate. If they create value domestically with US labor, they would have a low tax rate. The tax difference could be used to offset the labor cost advantage of offshored production.

It would take time, but jobs would come back to the US. Cities, states, and the federal government would slowly see their tax bases rebuilt. Consumer incomes would again rise with productivity, and the economy could be put back together.

As for the federal deficit, it could be significantly reduced by ending Washingtons wars. As various experts have established, these wars are extremely expensive, adding trillions of dollars to the financing needs of the US government. As other experts have shown, the wars do not benefit anyone but a narrow clique of military/security industries. Obviously, it is not democratic to destroy a peoples future for the sake of special interests.

Can these solutions be implemented or are the entrenched special interests too strong and too short-sighted?

There is no prospect of finding out when the financial press and economic commentators are immune to reality. Until the real situation is understood, nothing can be done. It is difficult to sell a solution when the problem is not recognized and understood. That is why I focus on explaining the problems.

John Devaney, named by Time magazine as one of the 25 people most responsible for the world's economic crisis has been spotted on holidays in Croatia.

The 42-year-old stock exchange expert was spotted aboard his yacht Dorothy Ann and has raised attention of locals in the southern town of Trogir and the the waters of the island of Solta as being masked all the time, with his face hidden.

As reported by daily newspaper Vecernji List, John Devaney is on holidays with his family.

Author

Author

Logged

Logged