Author

Author

|

Topic: Alarm - Cover Your Ass! (Read 9695 times) |

|

Hermit

Archon

Posts: 4289

Reputation: 8.91

Rate Hermit

Prime example of a practically perfect person

|

|

Re:Alarm - Cover Your Ass!

« Reply #15 on: 2006-12-19 13:10:23 » |

|

THE UNITED STATES IS INSOLVENT

Source: Financial Sense University

Authors: Dr. Chris Martenson

Dated: 2006-12-17

Noticed By: Sat (via Mo)

Minor Reformatting and Editing: Hermit

The End of Money

Prepare to be shocked.

The US is insolvent. There is simply no way for our national bills to be paid under current levels of taxation and promised benefits. Our federal deficits alone now total more than 400% of GDP.

That is the conclusion of a recent Treasury/OMB report entitled Financial Report of the United States Government [PDF] that was quietly slipped out on a Friday (2006-12-15), deep in the holiday season, with little fanfare. Sometimes I wonder why the Treasury Department doesnt just pay somebody to come in at 4:30 am Christmas morning to release the report. Additionally, Ive yet to read a single account of this report in any of the major news media outlets but that is another matter.

But, hey, I understand. A report is this bad requires all the muffling it can get.

In his accompanying statement to the report, David Walker, Comptroller of the US, warmed up his audience by stating that the GAO had found so many significant material deficiencies in the governments accounting systems that the GAO was unable to express an opinion on the financial statements. Ha ha! He really knows how to play an audience!

In accounting parlance, thats the same as telling your spouse Our checkbook is such an out of control mess I cant tell if were broke or rich! The next time you have an unexplained rash of checking withdrawals from that fishing trip with your buddies, just tell her that you are unable to express an opinion and see how that flies. Let us know how it goes!

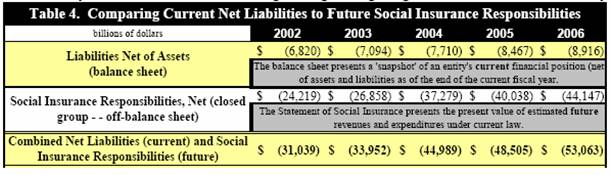

Then Walker went on to deliver the really bad news:Despite improvement in both the fiscal year 2006 reported net operating cost and the cash-based budget deficit, the U.S. governments total reported liabilities, net social insurance commitments, and other fiscal exposures continue to grow and now total approximately $50 trillion, representing approximately four times the Nations total output (GDP) in fiscal year 2006, up from about $20 trillion, or two times GDP in fiscal year 2000.

As this long-term fiscal imbalance continues to grow, the retirement of the baby boom generation is closer to becoming a reality with the first wave of boomers eligible for early retirement under Social Security in 2008.

Given these and other factors, it seems clear that the nations current fiscal path is unsustainable and that tough choices by the President and the Congress are necessary in order to address the nations large and growing long-term fiscal imbalance. Wow! I know David Walkers been vocal lately about his concern over our economic future but it seems almost impossible to ignore the implications of his statements above. From $20 trillion in fiscal exposures in 2000 to over $50 trillion in only six years? What shall we do for an encore

shoot for $100 trillion?

And how about the fact that boomers begin retiring in 2008

that always seemed to be waaaay out in the future. However, beginning January 1st we can start referring to 2008 as next year instead of some point in the future too distant to get concerned about now. Our economic problems need to be classified as growing, imminent, and unsustainable.

And let me clarify something. The $53 trillion shortfall is expressed as a net present value. That means that in order to make the shortfall disappear wed have to have that amount of cash in the bank today - earning interest (the GAO uses 5.7% & 5.8% as the assumed long-term rate of return). Ill say it again - $53 trillion, in the bank, today. Heck, I dont even know how much a trillion is let alone fifty-three of em.

And next year wed have to put even more into this mythical interest bearing account simply because we didnt collect any interest on money we didnt put in the bank account this year. For the record, 5.7% on $53 trillion is a bit more than $3 trillion dollars so you can see how the math is working against us here. This means the deficit will swell by at least another $3 trillion plus whatever other shortfalls the government can rack up in the meantime. So call it another $4 trillion as an early guess for next year.

Given how studiously our nation is avoiding this topic both in the major media outlets and during our last election cycle, I sometimes feel as if I live in a small mountain town that has decided to ignore an avalanche that has already let loose above in favor of holding the annual kindergarten ski sale.

The Treasury department soft-pedaled the whole unsustainable gigantic deficit thingy in last years report but they have taken a quite different approach this year. From page 10 of the report [PDF] (supra):The net social insurance responsibilities scheduled benefits in excess of estimated revenues) indicate that those programs are on an unsustainable fiscal path and difficult choices will be necessary in order to address their large and growing long-term fiscal imbalance.

Delay is costly and choices will be more difficult as the retirement of the baby boom gets closer to becoming a reality with the first wave of boomers eligible for retirement under Social Security in 2008 I dont know how that could be any clearer. The US Treasury department has issued a public report warning that we are on an unsustainable path and that we face difficult choices that will only become more costly the longer we delay.

Perhaps the reason US bonds and the dollar have held up so well is that we are far from alone in our predicament. In a recent article detailing why the UK Pound Sterling may fall, we read this horrifying evidence:Officially, [UK] public sector net debt stands at £486.7bn. That's equal to US$953.9bn and represents a little under 38% of annual GDP. Add the state's "off balance sheet" debt, however including its pension promises to state-paid employees and the total shoots nearly three times higher. Research by the Centre for Policy Studies in London says it would put UK government deficits at a staggering 103% of GDP. If we perform the same calculations for the US, however, we find that the official debt stands at $8.507 trillion or 65% of (nominal) GDP but when we add in our off balance sheet items the national debt stands at $53 trillion or 403% of GDP.

Now thats horrifying. Staggering. Whatever you wish to call it. More than four hundred percent of GDP(!). And thats just at the federal level. We could easily make this story a bit more ominous by including state, municipal and corporate shortfalls. But lets not do that.

Heres what the federal shortfall means in the simplest terms.[1] There is no way to grow out of this problem. What really jumps out is that the US financial position has deteriorated by over $22 trillion in only 4 years and $4.5 trillion in the last 12 months (see table below, from page 10 of the report [PDF] (supra)). The problem did not get better as a result of the excellent economic growth over the past 3 years but rather got worse and is apparently accelerating to the downside.

Any economic weakness will only exacerbate the problem. You should be aware that the budgetary assumptions of the US government are for greater than 5% nominal GDP growth through at least 2011. In other words, because no economic weakness is included in the deficit projections below, $53 trillion could be on the low side. Further, none of the long-term costs associated with the Iraq and Afghanistan wars are factored in any of the numbers presented (thought to be upwards of $2 trillion more).

[2] The future will be defined by lowered standards of living. As Lawrence Kotlikoff pointed out in his paper titled Is the US Bankrupt? posted to the St. Louis Federal Reserve website, the insolvency of the US will minimally require some combination of lowered entitlement payouts and higher taxes. Both of those represent less money in the taxpayers pockets and, last time I checked, less money meant a lower standard of living.

[3] Every government facing this position has opted to print its way out of trouble. Thats an historical fact and our country shows no indications, unfortunately, of possessing the unique brand of political courage required to take a different route. In the simplest terms this means you & I will face a future of uncomfortably high inflation, possibly hyperinflation if the US dollar loses its reserve currency status somewhere along the way.

Of course, it is impossible to print our way out of this particular pickle because printing money is inflationary and therefore a hidden tax on everyone. Consider, whats the difference between having half of your money directly taken (taxed) by the government and having half of its value disappear due to inflation? Nothing. Except that the former is political suicide while the second is conveniently never discussed by the US financial mainstream press (for some reason) and therefore goes undetected by a majority of people as the thoroughly predictable outcome of deficit spending. All printing can realistically accomplish is the preservation of some DC jobs and the decimation of the middle and lower classes. [Hermit: Assuming for a moment that there is such a thing as a middle class in the USA.] In summary, I am wondering how long we can pretend this problem does not exist. How long can we continue to buy stocks and flip houses, forget to save, pile up debt, import Chinese made goods, and export debt? Are these useful activities to perform while theres an economic avalanche bearing down upon us?

Unfortunately, I am not smart enough to know the answer. I only know that hoping a significant and mounting problem will go away is not a winning strategy.

I know that we, as a nation, owe it to ourselves to have the hard conversation about our financial future sooner rather than later. And I suspect that conversation will have to begin right here, between you and me because I cannot detect even the faintest glimmer that our current crop of leaders can distinguish between urgent and expedient.

What we need is a good, old-fashioned grassroots campaign.

In the meantime, I simply do not know of any way to fully protect oneself against the economic ravages resulting from poorly managed monetary and fiscal institutions. For what its worth, I am heavily invested in gold and silver and will remain that way until the aforementioned institutions choose to confront what is rather than whats expedient. This could be a very long-term investment.

Are you shocked?

|

With or without religion, you would have good people doing good things and evil people doing evil things. But for good people to do evil things, that takes religion. - Steven Weinberg, 1999

|

|

|

Hermit

Archon

Posts: 4289

Reputation: 8.91

Rate Hermit

Prime example of a practically perfect person

|

|

Re:Alarm - Cover Your Ass!

« Reply #16 on: 2006-12-31 17:11:01 » |

|

International Forecaster December 2006 (#4) - Gold, Silver, Economy + More

Source: http://www.theinternationalforecaster.com

Authors: Bob Chapman (email: International_forecaster@yahoo.com)

Dated: 2006-12-30

These are extracts from the International Forecaster newsletter for DECEMBER 2006 (#4) Vol. 10 No. 12-4

US MARKETS

Stupidity has become a mantra in America. Evidentially Americans like to be brainwashed. You explain how their government is lying to them and screwing them and they do not want to hear about it. Corporate CEOs, Wall Street, government economists and analysts do not get it, or dont want to get it. You tell these thinkers real inflation is over 10% and the answer you get is the Fed has tightened very aggressively and inflation is not going to be a problem. When you explain the issuance of money and credit that has been over 12% annualized for four years and has neutralized the beneficial affect of higher rates, they do not want to hear about it. Such truth might ruin their day or make them think there could be problems. The level of interest rates only tells half the story as we have just pointed out. The other half is the expansion or contraction of money and credit. Of course, the Fed, government, Wall Street, corporate America and its mouthpiece CNBC never want to talk about this. Every week a few others and we publish those statistics and we and two other publish estimated M3 figures. All the others are in a conspiracy of silence or they are too dumb to understand. Who cares if the total expansion of money and credit is running at 14%, not only in the US, but in the EU as well? ABS securities are only 7% below last years record and CDO issuance is running more than 65% above last year. International reserve assets are up almost 20% as central banks collect more and more fiat currencies, while they sell off their only real asset, gold. Foreigners are buying US Treasuries and Agencies, and have increased their participation at an annual rate of 15%. How can professionals conceivably believe money is tight or it is under control? They cannot tighten interest rates any further or stop creating more money and credit because the system will collapse. On the other hand if they do not raise rates the world will eventually flee from the dollar. If they lower them the dollar will collapse as will the world monetary system. Do not expect the Fed under Mr. Bernanke to do anything more or different than Sir Alan Greenspan did. The Fed doesnt and cant deal with the bubbles they have created. If they did they would have to raise interest rates to 14% or more and the economy would suffer a depression. The Fed is enmeshed in a trap of its own making.

What is happening now is the Fed is attempting to impose a bubble on a bubble, an exercise doomed to failure. At least that is what monetary history tells us. That means a continuing decline in the value of the dollar. If as we are now seeing other major currencies join in on the money and credit expansion that leaves gold and silver as the only safe harbors. That is why these other major currencies are doing what they are doing, and at the same time central banks are attempting to suppress gold. In the final analysis the Fed and other central banks simply cannot afford to tighten due to the current unserviceable debt. They have no choice but hyperinflation. This is why the upward moves in gold and silver are still after six years of a bull market only in their infancy.

Thus far easily available credit for mortgages and a ¾% drop in mortgage rates has temporarily slowed the decent of the real estate market. Stemming the tide doesnt end the flood. We do not see real estate prices rising anytime soon no matter what the Fed does. The psychology has been broken and it wont return for some time. Weak and weakening housing prices will weight heavily on the consumers ability to continue to spend even if energy prices remained at current levels. This set of circumstances will quickly affect corporate earnings and then be reflected in the stock and bond markets. That in turn will affect the use of credit and leverage, which will diminish. This is the very leverage that has boosted corporate earnings for more than four years and has assisted consumer spending. We have had bubbles in the stock market and in real estate. We have had major rallies in bonds and commodities. The only markets where overt suppression has taken place is in gold and silver. It is only a matter of time when there is a realization that they are the go to markets. Then the leveraged players will step in and ultimately create another bubble at much higher prices. Due mainly to massive US consumer and government debt and offshoring and outsourcing America and the dollar have been in decline for some time and will continue to decline unless offshoring and outsourcing are halted. In the meantime the balance of payments deficit worsens, as does the economy. That creates a relentless flight from the dollar. The elitists are forcing these changes, the result of which will be devastating for the US economy, as well as for the economies of Canada and Western Europe. The evolution of major growth for the past 25 years has been in the second and third world as the G7s share of global GDP has been shrinking. That shrinkage is now accelerating. All this did not happen by chance, it was planned that way. There is to be a leveling of all countries down to a common controllable level to usher in world government. That is what free trade and globalization is all about. Its about forced acceptance through diminishing economic and financial power. You had best discover what is being done to you and force your representatives to put a stop to it. If you do not you wont like the future the elitists have in store for you.

China, the second largest holder of US debt, reduced purchases of US bonds 1.7% in the first 10-months of the year. Central bankers in Venezuela, Indonesia and the UAE have said they will invest less of their reserves in dollar assets. South Korea and Romania say they prefer the higher yielding Fannie Mae and Freddy Mac paper.

US Treasury Secretary Henry Paulson, who represents the Goldman Sachs elitist program for China, is headed for a confrontation on China with the new-Democratic-controlled Congress after his fiasco in Beijing and word that he has softened on criticism of China. He said China was not a currency manipulator and, of course, they are, and everyone with any sense knows they are. The Democrats are going to call Paulson to Capital Hill to question him on the decision.

...

The depreciation of the US dollar, the worlds reserve currency, did not happen due to malfeasance its the result of a calculated plan to tax dollar users. The fall in the dollar is an indirect tax on all nations that trade with our country. The supply of dollars in modern times began in the 1960s with the birth of GATT in 1962, and later as WTO in 1986, and with the Vietnam War and the guns and butter economy. That was followed by the decompiling of the dollar from gold on 8/15/71, which officially made the dollar a fiat currency with no further gold backing. The foreign increase in dollar holdings as a result of LBJs Great Society and persistent US trade deficits set the stage for todays financial and economic quagmire, which has been exacerbated by free trade and globalization. Trade deficits are in essence a tax on those who trade with us. In 1971, the dumping of the gold standard was in reality a declaration of bankruptcy. What is very interesting is that it took only ten years for our system to collapse. Thus, America has extracted an enormous amount of economic goods from foreigners with no intention of paying for them. Being the dominant military power in the world no nation was prepared to challenge this indirect taxation or tribute. As of today the world continues to accept this taxation stoically.

In 1972 a deal was cut with Saudi Arabia. The US would support and protect this monarchical dictatorial government if the Saudis would only accept dollars for oil and in turn invest part of their income in US federal and agency debt and into Americas markets. Dollars became exchangeable for oil instead of gold. The world needed dollars because they had to buy oil. Once this changed the dollar would become totally fiat. That is what happened when the US crossed Saddam Hussein and he began selling oil in dollars. The US could not allow that. The power of the empire would be broken, the dollar, oil link would have been destroyed, thus invasion and occupation. The invasion was to stop oil sales in dollars and to steal the oil in the process. The war had nothing to do with human rights, WMD or spreading democracy. It was about keeping the dollar as the worlds imperial currency. The invasion was meant to show that the US would destroy anyone or any country that dared to not use the dollar in commerce. The US was defending its money monopoly.

Money and credit continue to expand aggressively. Total bank credit and M3 are expanding around 10%, y-o-y. Since the Fed enacted it's cost-cutting move in March 2006, presumably for the benefit of their private shareholders (And, yes the Fed is private entity), M3 has expanded from 8.5% to over 10%. Total bank credit has also expanded from 8.5 to over 10% over the same period. These numbers draw an erry comparison to the 2000 to 2001 credit and money growth rates, except this time M3 must be estimated. A real world analog for estimation is guess. This means the growth rates could be significantly higher.

We havent decided yet if Irans switch to euros from dollars was something the US wanted Iran to do. In all probability the answer is probably yes. This is the ultimate excuse to attack Iran. The elitists were very upset that Israel was beaten by Hezbollah in Lebanon, but even more upset that Israel was incapable of invading Syria and occupying that nation. If Israel had done so it would have severely weakened the insurgents in Iraq and brought an end to the conflict and occupation.

Irans switch to euros is the greatest threat yet to dollar supremacy. The case for an Iranian oil bourse in euros has essentially been bypassed. The usage of the euro is now universal in Iran and it will spread to other countries as well, thus we change our position. Iran has to be attacked by elitist US interests. They have no choice now. Just as an example, major oil producers such as Japan, India and China will be able to reduce dollar reserves as well as of Europe. This is a devastating blow to elitist dollar interests. A portion of dollar holdings by those who buy Iranian oil and gas can be converted to euros, other currencies and gold. The dollar would then drop 50% or more. Russia of course is a natural to dump dollars for euros because the majority of their trade is with Europe. The Gulf States are in the same boat.

...

GOLD, SILVER, PLATINUM, PALADIUM AND DIAMONDS

On Tuesday gold was up $4.60 coming out of Europe and after the Comex opening went up $9.60. It wasnt long before the gold suppression cartel snapped into action and we had to settle for a $4.20 gain to close at $623.80. Silver had been up $0.40 and closed up $0.078 to $12.50. The February gold contract rose $4.60 to $626.90, silver rose $0.09 to $12.73 and copper rose $0.02 to $2.88. Gold open interest rose 795 contracts to 341,890 with silver OI falling 880 contracts to 101,747, which is only 5,000 contracts off its multi-year low. On Friday Tocom the big gold shorts added only 114 contracts to be net short 118,532. On Monday they increased their shorts by 6 contracts to 118,548. Goldman covered 81 shorts on Friday and Monday for a net contraction to 31,790. They increased 114 contracts on Friday and on Monday they covered 61 contracts in silver to bring the total silver short to 3,646 contracts. It is interesting that Russias gold position on 12/31/05 was 369 tons and on 11/20/06 it was 400 tons. Gold reserves increased by 31 tons over 11 months, or about 2.8 tons per year. The HUI gained 1.87 to 329.89 and the XAU rose .86 to 138.45 on Tuesday. Tuesday saw holidays in Canada, the UK and parts of Europe.

It should interest you to know the silver production in Mexico dropped 41.5% in October YOY. Mexico is the worlds largest silver producer. October production fell to 4.5 M/oz. If the trend were to continue that would mean 54 million ounces annually down from more than 90 million ounces. Wed say that is very bullish for silver.

On Tuesday the Dow opened down and then spent the whole day to the upside finishing up 64 points to 12,408. The S&P rose 54 Dow points and Nasdaq rose 72 Dow points. Oil fell $1.31 to $61.10, gas fell $0.06 to $1.57 and natural gas fell $0.52 to $6.11. The euro fell .0037 to $1.2090, the pound fell .0054 to $1.95, the Canadian dollar fell .28 to 86.20 and the dollar index rose .12 to 83.79. Two year Treasury notes yielded 4.72% and the 10s yielded 4.60%.

The 24-karat American Buffalo gold coins have not proven that popular. After sales of 99,500 in June and 117,500 in July, sales have fallen dramatically. August saw 22,000 sold, September 33,500, October 21,500, November 10,000 and December 15,000. The sales this year of American Gold Eagles have been poor as well.

Russias gold production fell 1.6% YOY in January-November to 155.097 tons. Mine output fell 2.3% YOY to 139.92 tons.

Thirteen of 34 traders, investors and analysts surveyed from Sydney to Chicago on 12/22 advised buying gold, which rose 0.5% last week.

Investment in Street Tracks Gold Trust, the $9 billion exchange-traded fund linked to the price of gold, has more than doubled in value this year and the number of shares outstanding jumped 78%. Meanwhile the dollar has fallen 8% on the dollar index against a basket of six major currencies. The fund attracted $4.7 billion this year, up from $3 billion in 2005.

Gold should do very well in the first quarter of 2007, because the dollar should decline further. The market should top out and the economic and financial situation should worsen. Remember, all you hear about is the Dow being up 16% this year, but you do not hear that gold is up 22%. Contrarians should rejoice because the short-term gold timing newsletter index shows gold sentiment at 25 and that is where it was a year ago before gold rose 22%. We will likely get a repeat in 2007 and then some. That would put gold at $780 minimum.

|

With or without religion, you would have good people doing good things and evil people doing evil things. But for good people to do evil things, that takes religion. - Steven Weinberg, 1999

|

|

|

|

Logged

Logged