Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #15 on: 2008-11-25 23:53:43 »

[Fritz]Well it is nice to know we have some excitement to look forward to in North America assuming we get it.

Iceland Riots Precursor To U.S. Civil Unrest?

Demonstrators call for government to resign in wake of financial collapse

Source: Prison Planet Author: Paul Joseph Watson Date: Tuesday, November 25, 2008

Riots and protests in Reykjavik calling for the government of Iceland to resign have increased following a financial catastrophe that has wiped out half of the kronas value and put one third of the population at risk of losing their homes and life savings. Could similar scenes of civil unrest be repeated in the United States as the economy continues to implode?

It was the latest in a series of protests in the capital since Octobers banking collapse crippled the islands economy. At least five people were injured and Hordur Torfason, a well-known singer in Iceland and the main organiser of the protests, said the protests would continue until the government stepped down, reports the Scotsman.

As crowds gathered in the drizzle before the Althing, the Icelandic parliament, on Saturday, Mr Torfason said: They dont have our trust and they are no longer legitimate.

Hundreds more gathered in front of a local police station, pelting eggs at the windows, using a bettering ram to force the doors open and demanding the release of a protester.

A banner hung from a government building read Iceland for Sale: $2,100,000,000, the amount of the loan the country will receive from the IMF.

Gudrun Jonsdottir, a 36-year-old office worker, said: Ive just had enough of this whole thing. I dont trust the government, I dont trust the banks, I dont trust the political parties, and I dont trust the IMF.

We had a good country and they ruined it.

These arent the actions of unwieldy mobs in third world countries, were talking about a country that had one of the highest living standards in Europe and a relatively wealthy and sedate population, the vast majority of whom are now in revolt over mass redundancies and the fast disappearing values of their paychecks and savings.

More peaceful protests against the Federal Reserve during the End the Fed events over the weekend were largely ignored by the U.S. corporate media, but the potential for wider chaos exists should the dollar finally cave in to the hyperinflationary bubble that is being created by the ceaseless printing of money to fund the multi-trillion dollar bailout.

Those who continue to assert, It cant happen here, only need to look at the scenes in Reykjavik to realize that similar events could unfold across the U.S., where the reaction of militarized riot cops and even the military itself may be a little more heavy handed to say the least.

With top Russian analysts predicting the breakup of the U.S. into different parts, allied with people like deadly accurate trends forecaster Gerald Celente warning of food riots and tax rebellions, the scenes in Reykjavik may be amplified in the U.S. should a significant portion of the public wake up to the monumental fraud of the bailout and begin to feel the impact of its consequences as we enter 2009.

[Fritz]Well it is nice to know we have some excitement to look forward to in North America assuming we get it.

[Blunderov] It seems entirely possible that in the USA even more turbulence may ensue than has occurred in Iceland. Some while back I posted about how a whole bunch of US soldiers had been sent back home from Iraq for riot control training. This, mark you, from a battlefield where every soldier is desperately necessary - according to the powers that be in any case. Hmm. Just how much worse is this meltdown actually going to get? Angry people starving en masse in the streets bad maybe? Apparently somebody somewhere hasn't ruled this out...

Russian analyst predicts decline and breakup of U.S.

Global Research, November 25, 2008 RIA Novosti - 2008-11-24

A leading Russian political analyst has said the economic turmoil in the United States has confirmed his long-held view that the country is heading for collapse, and will divide into separate parts.

Professor Igor Panarin said in an interview with the respected daily Izvestia published on Monday: "The dollar is not secured by anything. The country's foreign debt has grown like an avalanche, even though in the early 1980s there was no debt. By 1998, when I first made my prediction, it had exceeded $2 trillion. Now it is more than 11 trillion. This is a pyramid that can only collapse."

The paper said Panarin's dire predictions for the U.S. economy, initially made at an international conference in Australia 10 years ago at a time when the economy appeared strong, have been given more credence by this year's events.

When asked when the U.S. economy would collapse, Panarin said: "It is already collapsing. Due to the financial crisis, three of the largest and oldest five banks on Wall Street have already ceased to exist, and two are barely surviving. Their losses are the biggest in history. Now what we will see is a change in the regulatory system on a global financial scale: America will no longer be the world's financial regulator."

When asked who would replace the U.S. in regulating world markets, he said: "Two countries could assume this role: China, with its vast reserves, and Russia, which could play the role of a regulator in Eurasia."

Asked why he expected the U.S. to break up into separate parts, he said: "A whole range of reasons. Firstly, the financial problems in the U.S. will get worse. Millions of citizens there have lost their savings. Prices and unemployment are on the rise. General Motors and Ford are on the verge of collapse, and this means that whole cities will be left without work. Governors are already insistently demanding money from the federal center. Dissatisfaction is growing, and at the moment it is only being held back by the elections and the hope that Obama can work miracles. But by spring, it will be clear that there are no miracles."

He also cited the "vulnerable political setup", "lack of unified national laws", and "divisions among the elite, which have become clear in these crisis conditions."

He predicted that the U.S. will break up into six parts - the Pacific coast, with its growing Chinese population; the South, with its Hispanics; Texas, where independence movements are on the rise; the Atlantic coast, with its distinct and separate mentality; five of the poorer central states with their large Native American populations; and the northern states, where the influence from Canada is strong.

He even suggested that "we could claim Alaska - it was only granted on lease, after all."

On the fate of the U.S. dollar, he said: "In 2006 a secret agreement was reached between Canada, Mexico and the U.S. on a common Amero currency as a new monetary unit. This could signal preparations to replace the dollar. The one-hundred dollar bills that have flooded the world could be simply frozen. Under the pretext, let's say, that terrorists are forging them and they need to be checked."

When asked how Russia should react to his vision of the future, Panarin said: "Develop the ruble as a regional currency. Create a fully functioning oil exchange, trading in rubles... We must break the strings tying us to the financial Titanic, which in my view will soon sink."

Panarin, 60, is a professor at the Diplomatic Academy of the Russian Ministry of Foreign Affairs, and has authored several books on information warfare.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #18 on: 2008-11-26 22:04:08 »

Quote:

[Blunderov]<snip>Hmm. Just how much worse is this meltdown actually going to get?<snip>

Interesting article thx. I'm not hearing much from your neck of the world. Is there any apparent fallout yet from the USA screw the world last one with all the "chicks for free money for nothing" event, aside from the inherent day to day struggles of the region ?

Quote:

[Blunderov] Meanwhile back at the ranch the keenest minds on the planet conclude that faith-based economics will save the day...

<snip> I'm not hearing much from your neck of the world. Is there any apparent fallout yet from the USA screw the world last one with all the "chicks for free money for nothing" event, aside from the inherent day to day struggles of the region ?</snip>

[Blunderov] I regret not being more active than I have been lately. Not only is moving to Cape Town rather like dropping off the edge of the world at the best of times, but I am engaged in a titanic struggle to whip my new accommodations, a half built house in Observatory (ping Walter:) ) into habitable shape. Skills I had long thought redundant (eg tiling, carpentry, locksmithing) have once again been called into play. I'm exhausted! Happy though.

And so it is that even local events mostly pass me by at the moment. Apparently the Springboks thrashed the English rugby team by a record score at Twickenham the other day and I only found out by accident a week later! Talk about 'out of the loop'. This would never have happened in Jo'burg.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #20 on: 2008-11-27 22:32:10 »

Quote:

[Blunderov] I regret not being more active than I have been lately. Not only is moving to Cape Town rather like dropping off the edge of the world at the best of times, but I am engaged in a titanic struggle to whip my new accommodations, a half built house in Observatory (ping Walter:) ) into habitable shape. Skills I had long thought redundant (eg tiling, carpentry, locksmithing) have once again been called into play. I'm exhausted! Happy though.

[Fritz]All the best in your adventure. I can empathize; my son just bought a real fixer upper, his first and a city apartment dweller to date has enlisted his old man to help resurrect the 1860 post a beam thing into a house. I have found muscles long since unused, we had to dig up the yard to find the well and bring it to the surface tunnel through 3 foot thick field stone foundations to get the plumbing inside, there may be hope I get back closer to my fighting weight (ya right).

The Observatory part sounds cool; some how a Comet discovered and called Blunderov seems right.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #21 on: 2008-11-27 22:37:59 »

[Fritz]Updates for the thread

Source: BBC news Author: NA Date: Tuesday, 25 November 2008

US Fed announces $800bn stimulus

Henry Paulson announces the stimulus package

The Federal Reserve is to inject another $800bn (�526.8bn) into the US economy in a further effort to stabilise the financial system.

US Treasury Secretary Henry Paulson said the stimulus package aimed to make more lending available to consumers.

About $600bn will be used to buy up mortgage-backed securities while $200bn is being targeted at unfreezing the consumer credit market.

Financial institutions are reluctant to lend, deepening the economic slowdown.

US BAIL-OUTS IN BRIEF 19 September: US officials start working on a $700bn plan to help rid US banks of bad debts 6 October: The Fed announces plans to buy massive amounts of short-term debt from companies in an effort to unfreeze the money markets 14 October: US government taps into the $700bn available to announce a $250bn plan to purchase stakes in a variety of banks 9 November: Insurance giant AIG gets fresh financial help from the US government, which brings the total aid package for the firm to about $150bn. 12 November: Authorities abandon plans to use some of the $700bn to buy up banks' bad debts. The bail-out fund will be used to buy shares in ailing lenders 25 November: A new $800bn stimulus package announced

Costly plan creates debt mountain US government bail-outs so far

The situation has been exacerbated as the credit crisis has worsened.

Meanwhile US President-elect Barack Obama said budget reform was "imperative" with the economy in crisis.

"It is not an option. It's a necessity," he said.

'Troubling'

Key lending such as credit cards, car loans and student loans had essentially come to a halt in October, Mr Paulson said. He added that the new measures were aimed at getting these types of lending back to more normal levels.

"It will take time to work through the difficulties in our market and our economy and new challenges will continue to arise," he said.

"We are committed to using all the tools at our disposal to preserve the strength of our financial institutions and stabilise our financial markets to minimise the spill-over into the rest of the economy."

The announcement came as Commerce Department figures showed US economic output shrank between July and September at a faster pace than initially predicted, which the White House described as "troubling".

GDP fell at an annual rate of 0.5% in the third-quarter - from the 0.3% estimated a month ago - as consumers cut spending by the largest amount in 28 years.

"This is why we are having to take such bold actions," a White House spokeswoman said.

THE $800BN BAIL-OUT

$100bn - Buying debts from Freddie Mac and Fannie Mae

$500bn - Buying mortgage-backed securities

$200bn - Lending to holders of debt backed by consumer loans

Meanwhile, the Standard & Poor's/Case-Shiller national home price index slumped by a record 16.6% during the quarter from the same period a year ago - taking prices down to levels not seen since early 2004.

Bail-out details

Under the latest rescue plan - which is in addition to the already-announced $700bn bank bail-out - the Fed is to buy up to $100bn in debt from the troubled mortgage giants Fannie Mae and Freddie Mac.

The central bank said it would also buy another $500bn in mortgage-backed securities - pools of mortgages that are bundled together and sold to investors.

The Fed said that the $600bn effort to support the mortgage market was being taken to reduce the cost of home mortgages and increase their availability.

They are getting to the heart of the problem, it's clean, it's quick, it's direct

Todd Abraham, Federated Investors

Obama vows to reform US budget

It said the purchases of the mortgages and mortgage-backed securities would take place over a number of months.

In addition to the $600bn effort on mortgages, the Fed also unveiled a separate programme to help unfreeze the consumer debt market.

The central bank said it would lend up to $200bn to the holders of securities backed by various types of consumer loans, such as credit cards and student loans.

Analyst reaction

News of the latest massive financial rescue plan was generally welcomed.

"They are getting to the heart of the problem, it's clean, it's quick, it's direct. It's a good way to bring down mortgage rates, because at the end of the day they have to stabilise the housing market," said Todd Abraham of Federated Investors, Pittsburgh.

Robert Macintosh, chief economist with Eaton Vance, Boston, said: "If they can pull it off it'll make some people happy, but I don't know how effective it'll actually be."

Scott Brown, chief economist at Raymond James Associates, Florida, said: "Here is the Fed taking a bunch of debt out of the market, which doesn't hurt. I think it should it should help unblock the credit markets."

The severe financial crisis that is rocking global markets at the moment began more than a year ago with rising defaults on sub-prime mortgages, loans provided to borrowers with weak credit histories.

<snip>The Observatory part sounds cool; some how a Comet discovered and called Blunderov seems right.</snip>

[Blunderov] In order for it to be true to form it would have to be a comet with an erratic orbit

Meanwhile the shit storm continues unabated.

AFAICT, the authorities are in effect simply printing money; nobody seriously expects these "loans" from the taxpayer to be paid back with anything other than toy money - if they are even ever paid back at all. This printing of money is a de facto devaluation of the currency. This something which is not likely to be to the taste of the USA's creditors but there is precious little they can do about it without cutting off their noses to spite their faces. America is shaping to become a Sampson pulling down the temple of the world economy around its own ears and quite understandably a lot of people want to get the hell away from there before this happens. Amongst other things, fewer and fewer countries are now interested in stumping up further soldiers and treasure to prop up American manufactured wars while that aggressor nation licks its self inflicted wounds and bails out its buddies in the ruling elite.

"The problems we face today cannot be solved by the minds that created them" Albert Einstein November 24, 2008 "Information Clearinghouse" -- Obama hasn't even been sworn in yet, and already the Wall Street cheerleaders are celebrating his first great triumph. According the pundits, the stock market staged a surprise 494 point rally on Friday because--get this--it was announced that Timothy Geithner would be appointed Obama's Treasury Secretary.

Timothy who?

What nonsense. The sudden turn-around in stocks had a lot more to do with short-covering than anything else, but don't let that get in the way of a good story. Even so, the last minute surge on the NYSE couldn't stop another week-long bloodbath that ended with the Dow and S&P 500 tumbling another 5 percent. That's not to say that Geithner is not bright and talented guy. He is; and so is his White House counterpart, Lawrence Summers. But the media hype is way overdone. Geithner doesn't drive the markets and he isn't "change you can believe in". In fact, he's a protege of Henry Kissinger, a member of the Council on Foreign Relations, and has the same political pedigree as his predecessor, Henry Paulson. They're both part of the ruling fraternity and their views of the world are nearly identical. There's no doubt that Geithner will be more competent and effective than Paulson but, then again, who wouldn't be? Paulson may be the biggest flop at Treasury since Andrew Mellon steered the country onto the reef during the Great Depression. The recent flap over the Troubled Assets Relief Program (TARP) just proves the point. After convincing Congress to pass a $700 billion bailout plan--by invoking the specter of economic Armageddon and martial law--the former G-Sax chairman proceeded to set up a program for buying back mortgage-backed securities (MBS) and other junk paper from his banking buddies. Paulson argued that removing the crappy loans would help the banks get back on their feet and start lending again. Of course, no one could really figure out how the process was going to be executed, but maybe that's just nit-picking. Fortunately, Paulson never got a chance carry out his plan. He was torpedoed by the stock market which plunged seven days in a row losing nearly 20 percent of its value until Paulson threw in the towel and did what 200 economists had suggested from the very beginning---buy preferred shares in the banks so they could rev-up their credit engines again.

Will Geithner be that stubborn? Not likely. And Paulson is a hard-nosed class warrior, too. Notice how every dime of the bailout has gone to banksters while all the efforts to provide relief to autoworkers, consumers or struggling homeowners have been blocked. Anyone who isn't in the upper 1 percent income bracket can forget about getting a helping hand.

Paulson shoveled $25 billion to Citigroup without even sending in the regulators to see if they were solvent or not. How smart was that? Citi's stock has dropped 93% from its all-time high in May 2007 and ended Friday at a measly $3.77 per share. Its market cap. has gone from $280 billion to a skinny $20 billion in less than a year. Without a lifeline from the government, they won't make it through December; the short-sellers will carve them up like a smoked ham. Will Paulson come to Citi's rescue with more public cash? Absolutely. So why won't he support a similar bailout for the Big Three auto-makers who employ nearly a million people?

There was a clue in Sunday's paper as to why Paulson is stiffing the car companies. According to UPI :

"GMAC Financial Services said Thursday it had applied to the U.S. Federal Reserve for bank holding company status, a step toward securing federal aid. The auto and home financing company said it had also submitted an application to the U.S. Treasury to participate in the Capital Purchase Program set up in the $700 billion financial firm bailout program known as the Emergency Economic Stabilization Act.

"As a bank holding company, GMAC would obtain increased flexibility and stability," the company said in a statement." (UPI)

So why would GMAC want to become a bank holding company if General Motors is headed for the chopping block? Could it be that the government is working out a secret deal with management to put the company through Chapter 11 (reorganization) just so it can crush the union and eliminate their pension and health care benefits in one fell swoop?

You bet. Car workers will be reduced to slave wages just like they are in sunny Alabama where sharecropping has moved indoors. And--no surprise--the Democrats are right on board with this labor-busting charade. The auto industry isn't going to be shut down. That's just more fear-mongering like the blather about martial law and WMD. Detroit is going to be transformed into a workers gulag; Siberia on Lake Michigan, which is why Paulson is withholding the $25 billion. It's plain old class warfare.

Paulson has tried to spread the myth that his bailout eased the credit crunch, but it's not true. The stress in the credit markets was caused by very precise factors (Libor, the TED Spread, OIS-Libor) which were intentionally allowed to rise to perilous levels so Paulson could coerce Congress into giving him his bailout loot. It wasn't until Congress caved in that the FED addressed those market indicators by (setting up a new facility and) providing an explicit government guarantee on commercial paper and money markets. That's what made Libor go down, not Paulson's misguided TARP program which did absolutely nothing.

So, Yes, the banks do need to be recapitalized. But, No, TARP did not address the specific conditions in the credit markets which were causing the problems. And, Yes, Congress is too blind to see that they were duped by a top-hat Wall Street land-shark who pulled the wool over their eyes and made off with $350 billion.

Geithner will never engage in the same cynical antics as Paulson. It was Paulson who set up the Super SIV (Structured Investment Vehicle) after 2 Bear Stearns hedge funds blew up so he could help Citigroup and other financial institutions pawn-off their off-balance sheets garbage to investors by placing the US treasury's seal of approval on the rotten paper; another shameless rip-off shrink-wrapped in the Stars and Stripes.

Paulson's "Hope Now" (1-888-995-HOPE) was another scam that was supposed to help banks and homeowners work out the details for a rate freeze on mortgage resets. Paulson assured the public that 500,000 homeowners would take advantage of the program which would dramatically reduce rate of foreclosures. As it stands, Hope Now hotline has provided counseling to just 36,000 borrowers. Representatives have suggested loan workouts for fewer than 10,000 of them, a small fraction of borrowers in need." (Earlier Subprime Rescue Falters; Wall Street Journal)

"Only 10,000 homeowners; and Paulson promised 500,000?

Another slight miscalculation. The real purpose of Hope Now was to derail Shiela Bair's FDIC from enacting a program that has a real chance of helping people stay in their homes. Paulson doesn't like that idea; after all, there's still plenty of freeway overpasses for people to sleep under.

Paulson also initiated "Project Lifeline", which targeted homeowners who were delinquent 90 days or more on their mortgages. Here's the run-down of how it works:

"Project Lifeline involves servicers sending letters to borrowers -- prime, Alt-A, or subprime, we're past pretense on that part -- who are very seriously delinquent (90 days or three payments down or more). The letter says that if the borrower contacts the servicer within ten days, agrees to homeowner counseling, and provides sufficient financial documentation that the servicer can consider a case-by-case, deep-analysis style modification of the mortgage terms, the servicer will agree to put the foreclosure process on hold for 30 days while the workout is considered. If the borrower fails to respond to the letter, foreclosure proceeds."

Ever heard of Project Lifeline? No one else has either. That's because it was just another one of Paulson's PR chimeras that passed into oblivion as soon as it served its purpose of making it look like the administration really gives a damn. That's a laugh.

ENTER GEITHNER

Geithner is nothing like Paulson. He's discreet, practical, non ideological and diplomatic. His job is to find a way to plug the holes in a banking system that is undercapitalized by a whopping $2 trillion dollars while trying to keep the broader economy from crashing to earth. He's already concocted a stimulus plan (with Summers help) that should be big enough to get the country through the first quarter of '09 ($700 billion), but it will take sustained government spending via infrastructure and green technologies programs to make up for the staggering losses to consumer spending. Expect the red ink to flow knee-deep from the purple mountains majesty all across the fruited plains, and pray that China and Japan keep buying US Treasurys or the country will face historic hyper-inflation.

Geithner knows that his mandate far exceeds his job description. Consumer confidence is at record lows because the public has lost faith in their institutions. The fear-mongering and the deception of the last 8 years have taken their toll; the pessimism is palpable. But market-based systems require confidence to function properly, otherwise people withdraw their savings and hoard their money. And that is exactly what is happening. We have entered a period of extreme risk aversion where there's been a steady run on the financial system; investors have pulled their money out of commercial paper, structured investments, money markets, corporate bonds, and securities. The markets are in a state of panic. Investors are moving into safe havens like Treasurys while consumers are cutting back on spending. The whole system is contracting. The same thing happened during the Great Depression. The similarities are stunning. In Jason Zweig's "1931 and 2008: Will Market history Repeat Itself" the author says:

"Over the two weeks ended Nov. 20, 2008, the Dow Jones Industrial Average fell 16%. Over the two weeks ended Nov. 20, 1931, the Dow fell 16%.

If you think that is scary, consider this: In the final five weeks of 1931, the Dow fell 20% further. Then it went on to lose yet another 47% before it finally hit rock-bottom on July 8, 1932

It is vital to realize that markets are never under some obligation to stop falling merely because they have already fallen by an ungodly amount. It also is vital to explore how bad the worst-case scenario can get and to think about how you would respond if it comes to pass.

When it comes to worst-case scenarios, 1931-1932 is it. When the Dow finally stopped going down, in July 1932, it had lost 88% in 36 months. At that point, only five of the roughly 800 companies that still survived on the New York Stock Exchange had lost less than two-thirds of their value from their peak in 1929." (Wall Street Journal)

Geithner's job is to restore confidence through transparency and consistency. No more lying. No more fudging the numbers to keep the public in the dark. Investors are already voting with their feet. It will take trust to get them to come back. Geithner has a clean slate to work with, but if he chooses Paulson's route--the path of deception--he'll fail, too. He's got one chance to make good; otherwise....To his credit, he has made statements confirming his determination to reform the system. This is what he said to Congress in recent hearings:

"The United States will have to have to undertake substantial reforms to our financial system. There was a strong case for reform before this crisis, our system was designed in a different era for a different set of challenges. But the case for reform is stronger today. Reform is important because a strong and resilient financial system is integral to the performance of any economy. ...I think the severity and complexity of this crisis makes a very compelling case for a broad and comprehensive reassessment of how we use regulation to achieve an appropriate balance between efficiency and civility. This is extremely complicated both in terms of the tradeoffs involved but also in terms of building the necessary consensus involved both here in the United States and around the world. It is going to require significant changes in the way we regulate and supervise financial securities; changes that in my view, need to go well-beyond modest adjustments to some of the specific capital charges in the existing capital regime as it applies to banks."

Good. Investors want rules, guidelines, supervision, regulations and most of all accountability. Justice should be the organizing principle in the financial system just as it is in the legal system. That means securities fraud has to be investigated and prosecuted. No free passes for banking mandarins and toffee-nose fund managers. Break the law and go to jail, just like Jeffrey Skilling. This is the biggest financial meltdown in US history and not one CEO or CFO has even been indicted. Instead, the SEC wastes its time harassing Dallas Maverick's owner Mark Cuban in a politically-motivated witch hunt. What a fiasco. Why not clean up the cesspool on Wall Street first. That's where the problem is and that's how one reestablishes credibility.

Then there's the heavy lifting of rebuilding financial markets while hedge fund redemptions are approaching 50 percent, corporate bonds have dropped by nearly half, commercial property is tanking, consumer spending is in the dumps, and the housing market continues to crumble. That's not an easy task. And, at the same time, banking behemoth Citigroup needs an immediate injection of capital just to maintain operations. Once again, the Treasury will assume a gigantic liability to avoid wider damage to the system. According to the Wall Street Journal:

"The federal government agreed Sunday to take unprecedented steps to stabilize Citigroup Inc. by moving to guarantee close to $300 billion in troubled assets weighing on the bank's books, according to people familiar with details of the plan.

Treasury has agreed to inject an additional $20 billion in capital into Citigroup under terms of the deal hashed out between the bank, the Treasury Department, the Federal Reserve, and the Federal Deposit Insurance Corp....

In addition to the capital, Citigroup will have an extremely unusual arrangement in which the government agrees to backstop a roughly $300 billion pool of its assets, containing mortgage-backed securities among other things. Citigroup must absorb the first $37 billion to $40 billion in losses from these assets. If losses extend beyond that level, Treasury will absorb the next $5 billion in losses, followed by the FDIC taking on the next $10 billion in losses. Any losses on these assets beyond that level would be taken by the Fed."

What a nightmare. In a conference call held last Friday, Citi's chief executive Vikram Pandit boasted that Citi "had a fantastic business model" and that "we are one of the best counterparties in the world based on our capital, and based on our liquidity." Indeed, Pandit can count on virtually limitless liquidity from this point on.

Also, keep in mind, that when 2 Bear Stearns hedge funds went belly up in July 2007, the experts all agreed that there were probably only $200 to $300 mortgage backed securities (MBS) in the whole system. Now we find out that there are $300 billion on Citi's balance sheet alone! More lies. In truth, there were more than $5 trillion in MBS created between 2000 and 2006. A large portion of those are held by banks. That means more trouble ahead.

YOU AIN'T SEEN NOTHING YET

So how will Geithner and Summers deal with the problems they'll be facing just two months from now?

They'll do whatever they need to do to stabilize the financial system and to get consumers spending again. That means at least another $2 trillion added to the ballooning national debt and some extremely dodgy ways of getting liquidity into the system.(With the Fed Funds rate already at 1 percent, monetary policy is limited)

Larry Summers, who will serve as Obama's chief economics advisor, summed up his plan like this to Bloomberg News:

"At first I believed that any stimulus package should be timely, targeted, and temporary. But the situation has deteriorated so significantly from that point that I would now go for speedy, substantial, and sustained over a several year interval."

But how will Summers get money into the system if monetary policy has been ineffective and the banks are not providing sufficient credit?

Economist Nouriel Roubini answers that question in his latest blog entry on Global EconoMonitor web-site:

"The Fed (will) directly purchase long term government bonds as a way of pushing downward their yield and thus reduce the yield curve spread. But even such action may not be very successful in world where such long rates depend as much as anything else on the global supply of savings relative to investment. Thus, even radical action such as outright Fed purchases of 10 or 30 year US Treasury bonds may not work as much as desired. (MW: In other words, the Fed will buy its own debt to control long-term rates)

Next, the Fed could make "outright purchases of corporate bonds (high yield and high grade); outright purchases of mortgages and private and agency MBS as well as agency debt; forcing Fannie and Freddie to vastly expand their portfolios by buying and/or guaranteeing more mortgages and bundles of mortgages; one could decide to directly subsidize mortgages with fiscal resources; the Fed (or Treasury) could even go as far as directly intervening in the stock market via direct purchases of equities as a way to boost falling equity prices. Some of such policy actions seem extreme but they were in the playbook that Governor Bernanke described in his 2002 speech on how to avoid deflation. They all imply serious risks for the Fed and concerns about market manipulation."

"Finally, the Fed could try to follow aggressive policies to attempt to prevent deflation from setting in: massive quantitative easing; such as letting the dollar weaken sharply, flooding markets with unlimited unsterilized liquidity; talking down the value of the dollar; direct and massive intervention in the forex to weaken the dollar." (MW: Intentionally weakening the dollar to spur consumer spending and exports)

The bottom line is that Geithner and Summers will have to recapitalize the banks and deal with the massive corporate defaults at the same time they initiate their strategy for pumping liquidity into the system to keep the economy limping along. It's a tall order and there's no guarantee of success.

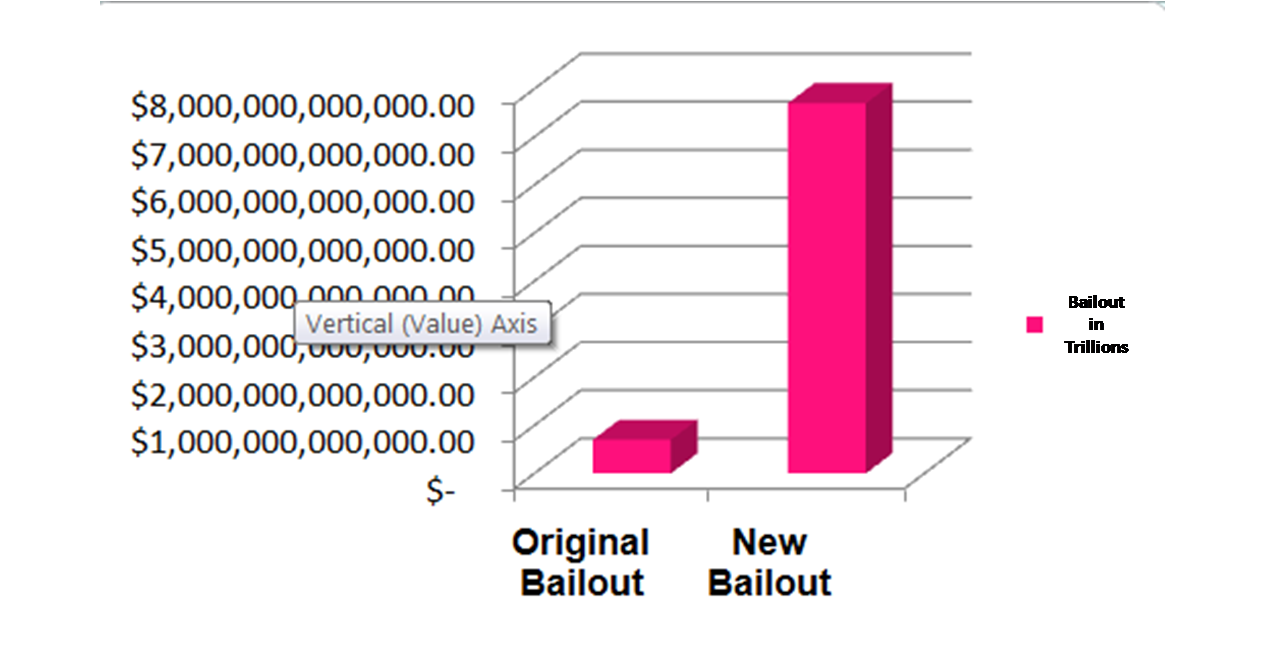

I missed this*. They've got a lot of what it takes to get along. The first column in the chart below represents the figure proposed to bail-out banks and credit institutions in TARP. The second represents the total amount that the US government is now committed to supplying to the same institutions.

Labels: banks, capitalism, credit, federal bail-out, tarp, us ruling class

U.S. Pledges Top $7.7 Trillion to Ease Frozen Credit (Update3) Email | Print | A A A

By Mark Pittman and Bob Ivry

Nov. 24 (Bloomberg) -- The U.S. government is prepared to provide more than $7.7 trillion on behalf of American taxpayers after guaranteeing $306 billion of Citigroup Inc. debt yesterday. The pledges, amounting to half the value of everything produced in the nation last year, are intended to rescue the financial system after the credit markets seized up 15 months ago.

The unprecedented pledge of funds includes $3.2 trillion already tapped by financial institutions in the biggest response to an economic emergency since the New Deal of the 1930s, according to data compiled by Bloomberg. The commitment dwarfs the plan approved by lawmakers, the Treasury Departments $700 billion Troubled Asset Relief Program. Federal Reserve lending last week was 1,900 times the weekly average for the three years before the crisis.

When Congress approved the TARP on Oct. 3, Fed Chairman Ben S. Bernanke and Treasury Secretary Henry Paulson acknowledged the need for transparency and oversight. Now, as regulators commit far more money while refusing to disclose loan recipients or reveal the collateral they are taking in return, some members of Congress are calling for the Fed to be reined in.

Whether its lending or spending, its tax dollars that are going out the window and we end up holding collateral we dont know anything about, said Congressman Scott Garrett, a New Jersey Republican who serves on the House Financial Services Committee. The time has come that we consider what sort of limitations we should be placing on the Fed so that authority returns to elected officials as opposed to appointed ones.

Too Big to Fail

Bloomberg News tabulated data from the Fed, Treasury and Federal Deposit Insurance Corp. and interviewed regulatory officials, economists and academic researchers to gauge the full extent of the governments rescue effort.

The bailout includes a Fed program to buy as much as $2.4 trillion in short-term notes, called commercial paper, that companies use to pay bills, begun Oct. 27, and $1.4 trillion from the FDIC to guarantee bank-to-bank loans, started Oct. 14.

William Poole, former president of the Federal Reserve Bank of St. Louis, said the two programs are unlikely to lose money. The bigger risk comes from rescuing companies perceived as too big to fail, he said.

Credit Risk

The government committed $29 billion to help engineer the takeover in March of Bear Stearns Cos. by New York-based JPMorgan Chase & Co. and $122.8 billion in addition to TARP allocations to bail out New York-based American International Group Inc., once the worlds largest insurer.

Citigroup received $306 billion of government guarantees for troubled mortgages and toxic assets. The Treasury Department also will inject $20 billion into the bank after its stock fell 60 percent last week.

No question there is some credit risk there, Poole said.

Congressman Darrell Issa, a California Republican on the Oversight and Government Reform Committee, said risk is lurking in the programs that Poole thinks are safe.

The thing that people dont understand is its not how likely that the exposure becomes a reality, but what if it does? Issa said. Theres no transparency to it so whos to say theyre right?

The worst financial crisis in two generations has erased $16 trillion, or 37 percent, of the value of the worlds companies since Sept. 15 and brought down three of the biggest Wall Street firms.

Markets Down

As of today, the Dow Jones Industrial Average is down 36 percent since the beginning of the year and 40 percent from its peak on Oct. 9, 2007. The S&P 500 fell 42 percent from the beginning of the year through today and 46 percent from its peak on Oct. 9, 2007. The Nikkei 225 Index has fallen 48 percent from the beginning of the year through today and 58 percent from its most recent peak of 18,261.98 on July 9, 2007. Goldman Sachs Group Inc. is down 73 percent, to $67.42, today from its peak of $247.92 on Oct. 31, 2007, and 69 percent this year.

Regulators hope the rescue will contain the damage and keep banks providing the credit that is the lifeblood of the U.S. economy.

Most of the spending programs are run out of the New York Fed, whose president, Timothy Geithner, is said to be President- elect Barack Obamas choice to be Treasury Secretary.

They Got Snookered

The money thats been pledged is equivalent to $24,000 for every man, woman and child in the country. Its nine times what the U.S. has spent so far on wars in Iraq and Afghanistan, according to Congressional Budget Office figures. It could pay off more than half the countrys mortgages.

Its unprecedented, said Bob Eisenbeis, chief monetary economist at Vineland, New Jersey-based Cumberland Advisors Inc. and an economist for the Atlanta Fed for 10 years until January. The backlash has begun already. Congress is taking a lot of hits from their constituents because they got snookered on the TARP big time. Theres a lot of supposedly smart people who look to be totally incompetent and its all going to fall on the taxpayer.

President Franklin D. Roosevelts New Deal of the 1930s, when almost 10,000 banks failed and there was no mechanism to bolster them with cash, is the only rival to the governments current response. The savings and loan bailout of the 1990s cost $209.5 billion in inflation-adjusted numbers, of which $173 billion came from taxpayers, according to a July 1996 report by the U.S. General Accounting Office, now called the Government Accountability Office.

Worst Crisis

The 1979 U.S. government bailout of Chrysler consisted of bond guarantees, adjusted for inflation, of $4.2 billion, according to a Heritage Foundation report.

The commitment of public money is appropriate to the peril, said Ethan Harris, co-head of U.S. economic research at Barclays Capital Inc. and a former economist at the New York Fed. U.S. financial firms have taken writedowns and losses of $666.1 billion since the beginning of 2007, according to Bloomberg data.

This is the worst capital markets crisis in modern history, Harris said. So you have the biggest intervention in modern history.

Bloomberg has requested details of Fed lending under the U.S. Freedom of Information Act and filed a federal lawsuit against the central bank Nov. 7 seeking to force disclosure of borrower banks and their collateral.

Collateral is an asset pledged to a lender in the event a loan payment isnt made.

Thats Counterproductive

Some have asked us to reveal the names of the banks that are borrowing, how much they are borrowing, what collateral they are posting, Bernanke said Nov. 18 to the House Financial Services Committee. We think thats counterproductive.

The Fed should account for the collateral it takes in exchange for loans to banks, said Paul Kasriel, chief economist at Chicago-based Northern Trust Corp. and a former research economist at the Federal Reserve Bank of Chicago.

There is a lack of transparency here and, given that the Fed is taking on a huge amount of credit risk now, it would seem to me as a taxpayer there should be more transparency, Kasriel said.

Bernankes Fed is responsible for $4.7 trillion of pledges, or 61 percent of the total commitment of $7.7 trillion, based on data compiled by Bloomberg concerning U.S. bailout steps started a year ago.

Too often the public is focused on the wrong piece of that number, the $700 billion that Congress approved, said J.D. Foster, a former staff member of the Council of Economic Advisers who is now a senior fellow at the Heritage Foundation in Washington. The other areas are quite a bit larger.

Fed Rescue Efforts

The Feds rescue attempts began last December with the creation of the Term Auction Facility to allow lending to dealers for collateral. After Bear Stearnss collapse in March, the central bank started making direct loans to securities firms at the same discount rate it charges commercial banks, which take customer deposits.

In the three years before the crisis, such average weekly borrowing by banks was $48 million, according to the central bank. Last week it was $91.5 billion.

The failure of a second securities firm, Lehman Brothers Holdings Inc., in September, led to the creation of the Commercial Paper Funding Facility and the Money Market Investor Funding Facility, or MMIFF. The two programs, which have pledged $2.3 trillion, are designed to restore calm in the money markets, which deal in certificates of deposit, commercial paper and Treasury bills.

Lehman Failure

Money markets seized up after Lehman failed, said Neal Soss, chief economist at Credit Suisse Group in New York and a former aide to Fed chief Paul Volcker. Lehman failing made a lot of subsequent actions necessary.

The FDIC, chaired by Sheila Bair, is contributing 20 percent of total rescue commitments. The FDICs $1.4 trillion in guarantees will amount to a bank subsidy of as much as $54 billion over three years, or $18 billion a year, because borrowers will pay a lower interest rate than they would on the open market, according to Raghu Sundurum and Viral Acharya of New York University and the London Business School.

Congress and the Treasury have ponied up $947 billion in TARP and other funding, or 12 percent.

The Federal Housing Administration, overseen by Department of Housing and Urban Development Secretary Steven Preston, was given the authority to guarantee $300 billion of mortgages, or about 4 percent of the total commitment, with its Hope for Homeowners program, designed to keep distressed borrowers from foreclosure.

Federal Guarantees

Most of the federal guarantees reduce interest rates on loans to banks and securities firms, which would create a subsidy of at least $6.6 billion annually for the financial industry, according to data compiled by Bloomberg comparing rates charged by the Fed against market interest currently paid by banks.

Not included in the calculation of pledged funds is an FDIC proposal to prevent foreclosures by guaranteeing modifications on $444 billion in mortgages at an expected cost of $24.4 billion to be paid from the TARP, according to FDIC spokesman David Barr. The Treasury Department hasnt approved the program.

Bernanke and Paulson, former chief executive officer of Goldman Sachs, have also promised as much as $200 billion to shore up nationalized mortgage finance companies Fannie Mae and Freddie Mac, a pledge that hasnt been allocated to any agency. The FDIC arranged for $139 billion in loan guarantees for General Electric Co.s finance unit.

Automakers Struggle

The tally doesnt include money to General Motors Corp., Ford Motor Co. and Chrysler LLC. Obama has said he favors financial assistance to keep them from collapse.

Paulson told the House Financial Services Committee Nov. 18 that the $250 billion that had already been allocated to banks through the TARP is an investment, not an expenditure.

I think it would be extraordinarily unusual if the government did not get that money back and more, Paulson said.

In his Nov. 18 testimony, Bernanke told the House Financial Services Committee that the central bank wouldnt lose money.

We take collateral, we haircut it, it is a short-term loan, it is very safe, we have never lost a penny in these various lending programs, he said.

A haircut refers to the practice of lending less money than the collaterals current market value.

Requiring the Fed to disclose loan recipients might set off panic, said David Tobin, principal of New York-based loan-sale consultants and investment bank Mission Capital Advisors LLC.

Mark to Market

If you mark to market today, the banking system is bankrupt, Tobin said. So what do you do? You try to keep it going as best you can.

Mark to market means adjusting the value of an asset, such as a mortgage-backed security, to reflect current prices.

Some of the bailout assistance could come from tax breaks in the future. The Treasury Department changed the tax code on Sept. 30 to allow banks to expand the deductions on the losses banks they were buying, according to Robert Willens, a former Lehman Brothers tax and accounting analyst who teaches at Columbia University Business School in New York.

Wells Fargo & Co., which is buying Charlotte, North Carolina-based Wachovia Corp., will be able to deduct $22 billion, Willens said. Adding in other banks, the code change will cost $29 billion, he said.

The rule is now popularly known among tax lawyers as the Wells Fargo Notice, Willens said.

The regulation was changed to make it easier for healthy banks to buy troubled ones, said Treasury Department spokesman Andrew DeSouza.

House Financial Services Committee Chairman Barney Frank said he was angry that banks used the money for acquisitions.

The only purpose for this money is to lend, said Frank, a Massachusetts Democrat. Its not for dividends, its not for purchases of new banks, its not for bonuses. There better be a showing of increased lending roughly in the amount of the capital infusions or Congress may not approve the second half of the TARP money.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #24 on: 2008-12-02 01:00:43 »

[Blunderov] Look, I admit that numbers are not my thing; I'm better with words. But when numbers get into the trillions they become downright unfriendly; I begin to get the distinct sensation that I'm losing grip, that reality is sliding from my ken. The derivatives bubble involves very many "trillions". The consequences may well be truly unimaginable.

Swap Defaults: The Next Installment of the Financial Crisis Posted in Main Blog (All Posts) on December 1st, 2008 5:36 am by HL

Swap Defaults: The Next Installment of the Financial Crisis

No one wants to talk about what will happen when our Wall Street Masters of the Universe cant pay off on their massive gambling debts in the derivatives markets. It looks like this really serious problem is just one more can being kicked down the road to the Obama administration. Is anyone ready to think about it yet?

What will happen if the derivative markets collapse? This is the question we dont seem to be asking in public. Maybe the answer is too scary. Take a deep breath and read this (thanks a lot, EW).

Remember the basics about credit default swaps. One side buys protection against loss on debt issued by a specified company or nation from the other. The buyer doesnt even have to own the debt. It just pays a premium based on market assessment of risk. The seller gets the premium, and promises to pay the difference between the face value of the debt and the value at the date of a credit event, like bankruptcy or failure to make payments.

Take another deep breath. The ISDA gives the following estimate:

As of December 2007, gross mark-to-market value of all derivatives was approximately 2.4 percent of notional amount outstanding. In addition, net credit exposure (after netting but before collateral) is 0.5 percent of notional amount outstanding. Applying these percentages to the total ISDA Market Survey notional amount outstanding of $531.2 trillion as of June 30, 2008, gross credit exposure before netting is estimated to be $12.7 trillion and credit exposure after netting, but before collateral, is estimated to be $2.7 trillion.

Banks are big players in this stuff. Citigroup has a total portfolio of swaps of various kinds of a sickening $36.8tn. Oops, maybe another deep breath. The largest part of these are interest rate swaps, but it has sold $1.57tn and bought $1.67tn in notional amounts of CDSs, according to the chart on page 40 of Citis financial statements. The total portfolio of swaps is about 6.9% of all swaps outstanding.

If we take Citis portfolio profile to be reasonably like the overall market, which is reasonable because its so big, we could guess that its exposure to loss is .5% of the notional value of its portfolio, which is $184bn after netting and before application of collateral. Lets hope its only that bad.

Citi is required to evaluate its portfolio of derivatives using FASB rules. Citi provides a table of mark-to-market values for its trading portfolio. This gives values of $165bn and $149bn. There is much uncertainty here. For example, if Citi has hedged its protection sales with protection purchases on the same reference entities, it has to guess how much it can collect from its counterparties. It has to estimate where the losses on protection sales will occur, and where its bets on protection purchases will pay off. That cant be estimated easily, and Citi will use very conservative estimates internally. The financial statements are confusing on this point, as hedging, netting, and collateral are all lumped together for the entire portfolio of derivatives, including the enormous interest swap portfolio.

In an earlier diary, I suggested we impose a punitive tax on naked CDSs. Now I see that taxing wont work. Most of the players in this market look like Citi, with both purchases and sales of protection. If we tax gains, there wont be enough money for losers to pay winners, and the problem will be worse. A lot of gamblers are buyers and sellers, not on the same reference creditors, perhaps, and they will need money from the wins to pay off the losses. Crushing the transactions will also affect the ability of the sellers of protection to pay off on hedging transactions, which is probably important. For example, GM has used some of these to protect its pension plan.

Whalen offers another solution: make them all unenforceable. He suggests that one way to do this is bankruptcy of the big protection sellers, like AIG. He points out what we already know, that a lot of the money we sent to AIG is now posted as collateral with its CDS counterparties. How will we feel about this, he asks:

Remember, only a small portion of these positions are actually hedging exposure in the form of the underlying securities. The rest are speculative, in some cases 10, 20 of 30 times the underlying basis. Yet the position taken by Treasury Secretary Paulson and implemented by Tim Geithner (and the Fed Board in Washington, to be fair) is that these leveraged wagers should be paid in full.

Whalen thinks we should pay the hedging transactions in full, and pay pennies to the gamblers. Theoretically, this could be done in bankruptcy. In Chapter 11, the goal is to create a Plan of Reorganization which changes the obligations of the company to its creditors so that the reorganized company can succeed. The plan of reorganization would put hedging CDSs into one class, and naked CDSs into another. The hedge class would be paid close to par. The other would get a penny on the dollar. The plan has to be approved after a hearing in the bankruptcy court, and the gambling crowd will either eat the problem, or emerge from the shadows to object, which will expose their shabby game to national derision.

There are several big problems with this. First, when a bankruptcy is filed, there is usually an automatic stay, which stops creditors from taking action to obtain property of the Debtor. 11 U.S.C. §560 says that this doesnt apply to swaps. Other sections of the Bankruptcy Code do the same thing about other derivatives. The effect of these provisions is hard to predict, but they will make it difficult to stop counterparties from making a big fuss and probably limiting the ability of the company to protect itself and real creditors from the wolves.

Second, this solution doesnt solve the problem of gamblers who need their winnings to pay their losses. We may be bankrupting a whole lot of people and companies, and we wont know who until the bankruptcies start. Finally, bankruptcy wont work with banks and insurance companies that wrote CDSs themselves, as opposed to holding companies or sister companies. Notice that Citibank has written a bunch of protection. When banks and insurance companies go bankrupt, they are administered by the FDIC or the State Insurance Commissioner. In either case, there is a statutory order for payment of creditors, and it isnt likely that a court can do much about that order.

Im beginning to think that we should just terminate naked credit default swaps outright. Declare them illegal and unenforceable. This is just the first step, as there are loads of problems, like, what happened to the premiums.

Unfortunately, right now, the only people trying to come up with an answer are some fringe guys running around with their hair on fire. Our Masters in financial world are too busy demanding ransom from the government; they cant be expected to acknowledge the problem, let alone deal with it.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #25 on: 2008-12-03 14:32:37 »

Quote:

[Blunderov]<snip>Unfortunately, right now, the only people trying to come up with an answer are some fringe guys running around with their hair on fire. Our Masters in financial world are too busy demanding ransom from the government; they cant be expected to acknowledge the problem, let alone deal with it.<snip>

[Fritz]HEY ! ... Is he talking about us ? ... good thing my high testosterone level has rendered me mostly hairless.

Quote:

[Blunderov] Look, I admit that numbers are not my thing; I'm better with words. But when numbers get into the trillions they become downright unfriendly;<snip>

[Fritz]In agreement; peering down into my backup account after having shod the family and extended family vehicles with snow tires, hoarded some gas for the snow blower, put new battery into the old tractor and hoarded some diesel fuel for that ....an ever so tiny part of the trillions would make winter so much more fun and Christmas oh so much more merry ... ho ho ho....

Bailout costs more than Marshall Plan, Louisiana Purchase, moonshot, S&L bailout, Korean War, New Deal, Iraq war, Vietnam war

Bailout costs more than Marshall Plan, Louisiana Purchase, moonshot, S&L bailout, Korean War, New Deal, Iraq war, Vietnam war, and NASA's lifetime budget -- *combined*!

In doing the research for the "Bailout Nation" book, I needed a way to put the dollar amounts into proper historical perspective.

If we add in the Citi bailout, the total cost now exceeds $4.6165 trillion dollars.

People have a hard time conceptualizing very large numbers, so lets give this some context. The current Credit Crisis bailout is now the largest outlay In American history.

Crunching the inflation adjusted numbers, we find the bailout has cost more than all of these big budget government expenditures combined:

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #26 on: 2008-12-20 20:07:34 »

The sobering part is for Ontario and Canada we are on the hook for 20% of the bailout, and Ontario's total budget is not much more the $100 billion ... so will they cut health care or French language initiatives .... oh 'Au contrair, mon ami' .... just eat more snails and garlic to be healthier.

Sigh

Fritz

Bush announces automaker bailout

Source: radionetherland Author: n/a Date: Friday 19 December 2008 22:16 UTC

US President George W. Bush says the government will provide up to 17.4 billion dollars in emergency loans to ailing car manufacturers to prevent them from collapsing. The funds will go to General Motors and Chrysler. Ford has indicated it doesn't need aid at this point. The president stressed that the companies will be required to restructure and demonstrate their viability by 31 March.

The news comes as Russia announced similar measures to protect its car industry. The government will give individuals and firms discounts if they buy Russian cars. The government will also help pay for the transportation of Russian cars to the east of the country so people won't buy automobiles imported from neighbouring Japan.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #27 on: 2008-12-26 20:37:23 »

Source: Economist Author: The Economist print edition Date: Dec 18th, 2008

Credit Crunch board game

You will need:

The board from the centre of The Economists Christmas issue (or pdf version of board below)

These rules

Risk cards, currency and icons from the pdfs below (or you can use your diamond cufflinks, or any other mementos of your former wealth, to represent you on the board)

Four coins

Scissors (to cut out currency and cards)

Three or more players; probably six at most Scissors (to cut out currency and cards)

Three or more players; probably six at most

How it works

Players start with 500m econos each. One player doubles as banker.

Players move round by throwing four coins and progressing as many squares as they throw heads. If a player throws four heads, he moves forward four spaces and has another turn; if he throws four tails, he throws again. When a player lands on a + square, he collects money from the bank; equally, when he lands on a minus square, he pays the bank.

The aim is to be the last solvent player. In order to achieve this, players try to eliminate the competition. Risk cards encourage players to pick on each other.

Players who cannot pay their fines may borrow from each other at any rate they care to settle onfor instance, 100% interest within three turns. They should negotiate with the other players to get the best rate possible. Players who cannot borrow must either go into Chapter 11 or be taken over.

Players may conceal their assets from each other. Chapter 11

When a player gets into debt and cant persuade anybody else to lend to him, he goes bankrupt. A player who goes bankrupt three times is eliminated.

A bankrupt player must move to the Chapter 11 cell and stay there until:

1. He uses a Get out of Chapter 11 card

2. He rolls four heads or four tails during his turn

3. He is taken over

A player coming out of bankruptcy goes to START.

If a player cannot escape Chapter 11 for five turns he is eliminated.

Takeover

A player may be taken over either if he cannot pay his debts or if he is already in Chapter 11. The purchaser pays the purchased players debts. If there is a takeover battle, the aspiring purchasers must bid against each other, and the highest bidder pays his bid to the bank.

The purchaser and subsidiary then play, in effect, as a team, though the purchaser is in charge. He gets to choose the beneficiaries and victims of the risk cards his subsidiary picks and may use the subsidiarys assets to pay his fines, or pay the subsidiarys fines if he wishes. But he does not have to: if his subsidiary gets into debt again, he can let the subsidiary go into Chapter 11. The subsidiary is then a free agent once more, and may get out of Chapter 11 in the usual ways. But the player who has just abandoned him may not take him over during that stay in Chapter 11, although he may during a subsequent visit.

Printing money

The Bank of Econia supplies the currency for this game. To access the banks vaults, download and print the money using the currency pdfs. Money may be printed in colour or grayscale.

The econo is available in five notes: Ec 10 million (here), Ec 50 million (here), Ec 100 million (here), Ec 500 million (here) and Ec 1000 million (here). There is a pdf page for each denomination with 10 bills on each page.

The Bank encourages a print run of:

60 x Ec 10m (6 pages with 10 bills on each page)

60 x Ec 50m (6 pages with 10 bills on each page)

60 x Ec 100m (6 pages with 10 bills on each page)

20 x Ec 500m (2 pages with 10 bills on each page)

20 x Ec 1000m (2 pages with 10 bills on each page)

Use scissors to separate notes.

Printing Financial Risk cards

There are 30 Financial Risk cards contained in three pdfs (here, here and here). Print one copy of each pdf and use scissors to separate cards. Place separated cards in a pile face down during play.

Printing icons

Players may choose any item to represent them on the board. Optional icons are contained on an icon pdf (here). Print page and separate desired icons using scissors. Fold back base flaps in order to allow the icon to stand upright.

Printing game board

The game board is available for printing on two pdfs (here and here) with one half of the board on each file.

Enlarging the board is encouraged. This may require utilising larger paper or printing then assembling the board from several pages.

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #28 on: 2008-12-30 10:41:47 »

Deepening economic strife in the US could lead to civil unrest and violence that would require military intervention, warns a new report from the US Army War College

"Widespread civil violence inside the United States would force the defense establishment to reorient priorities in extremis to defend basic domestic order and human security," writes Nathan Freier, a 20-year Army veteran and visiting professor at the college.

A copy of the 44-page report, "Known Unknowns: Unconventional 'Strategic Shocks' in Defense Strategy Development," can be downloaded here. Freier notes that his report expresses only his own views and does not represent US policy, but it's certain that his recommendations have come before at least some Defense Department officials.

The author warns potential causes for such civil unrest could include another terrorist attack, "unforeseen economic collapse, loss of functioning political and legal order, purposeful domestic resistance or insurgency, pervasive public health emergencies, and catastrophic natural and human disasters." The situation could deteriorate to the point where military intervention was required, he argues..

"Under these conditions and at their most violent extreme," he concludes, "civilian authorities, on advice of the defense establishment, would need to rapidly determine the parameters defining the legitimate use of military force inside the United States."

While the scenario presented is "likely not an immediate prospect," Freier concedes, it deserves consideration. Prior to 9/11, no one in the defense establishment would have envisioned a plot to topple skyscrapers with airliners, and the military should not be caught so off-guard again, he says.

To the extent events like this involve organized violence against local, state, and national authorities and exceed the capacity of the former two to restore public order and protect vulnerable populations, DoD would be required to fill the gap," he writes. "This is largely uncharted strategic territory."

Freier's report has merited some concern as it comes alongside revelations that the Defense Department has assigned a full-time Army unit to be on-call for domestic deployment.

An article in Monday's El Paso Times notes that military and police officials in Texas are unaware of team-up efforts such as those suggested in the report.

Arizona authorities told the Phoenix Business Journal they are similarly unaware of any new plans, although the Phoenix Police Department made clear its officers "always train to prepare for any civil unrest issue."

The Posse Comitatus Act restricts the military's role in domestic law enforcement, but it does not completely preclude involvement in cases of emergency or when emergency law is declared. As of now, though, such scenarios seem unlikely.

The bulk of Freier's report recommends refocusing Defense Department strategy toward thinking outside the box, in general, and the unlikely possibility of domestic deployments is just one longshot example he uses to illustrate a worst case scenario.

With or without religion, you would have good people doing good things and evil people doing evil things. But for good people to do evil things, that takes religion. - Steven Weinberg, 1999

Re:Jump You Fuckers: Follow the bouncing 700 Billion

« Reply #29 on: 2009-01-25 22:29:41 »

Enjoy

Cheers

Fritz

Citigroup A house built on Sandy

Source: The Economist Author: The Economist print edition Date: Jan 15th 2009

And the rain descended, and the floods came, and the winds blew, and beat upon that house; and it fell: and great was the fall of it

Illustration by S. Kambayashi

TOO big to fail, too shit to buy is the way some Citigroup insiders describe their employer. Not for much longer. On January 13th Citigroup announced that it had reached a deal to spin out Smith Barney, its broking arm, into a joint venture with Morgan Stanleys broker. The agreement presages even more dramatic changes. The bank has brought forward its fourth-quarter results to January 16th and expectations are high that Vikram Pandit, Citis chief executive, will unveil plans to slim the bank further and faster.

The Smith Barney deal is already a watershed. As recently as November, Mr Pandit heaped praise on the broker and said he did not want to sell it. No wonder. Citis wealth-management business, of which Smith Barney is a big part, was the only one of its main divisions to post a profit in the third quarter. And it sat snugly with Citis universal-bank model, endorsed by Mr Pandit just weeks ago, of offering a full array of services to customers. Click here

Citi will still receive its share of revenue from the joint venture, which overtakes the troubled Bank of America-Merrill Lynch combination as the worlds largest broker by number of advisers, but there is no question who will be in charge. Morgan Stanley is paying Citi $2.7 billion to take a 51% stake in the venture, which will be called Morgan Stanley Smith Barney, and has an option to take further stakes. James Gorman, now seen as favourite eventually to succeed John Mack as Morgan Stanleys boss, will be the ventures chairman.

Mr Pandits about-face reflects Citis continuing need for capital. Those quarterly results are expected to be the fifth in a row where Citi bosses own up to a loss. Although the bank has received two shots of government money and has a decent level of capital by some measures, its first line of defence, common equity, is thin. Mounting problems in its consumer and corporate loans, as well as some old wounds in its portfolio of mortgage-backed securities, threaten to erode it further. Selling Smith Barney, which creates tangible common equity of approximately $6.5 billion, is the quickest way of plugging the gap.

Gap-plugging alone does not constitute a strategy. Initial word of the deal sent Citis share price skidding on January 12th, as investors reasoned that the bank must be desperate if it was choosing to sell one of its best assets. Hence reports that more radical surgery is coming, with up to one-third of the banks assets being hived off to leave a slimmer Citi, focused on global corporate and retail banking.

Precisely what Mr Pandit has in mind is not clear, but it may be too late for an elegant retreat. Many of the businesses he would like to unload, such as Primerica, a seller of insurance, have been on the chopping-block for a while. Appetite will probably be keenest for the things that Citi would most like to keepits retail-banking operations in Mexico and South Korea, say, or its suddenly sexy transaction-processing business. There is talk of setting up a separate entity to house the assets earmarked for sale, which could then be divested later. But that would still leave Citi with the problem of how to fill todays holes in its capital.

Citis burst of activity signals two big, and necessary, shifts in thinking. The first is the final abandonment of the idea that has animated Citigroup since Sandy Weill engineered the merger of his company, Travelers, with Citicorp in 1998that of the financial supermarket. The news on January 9th that Robert Rubin, a powerful voice in favour of the universal model, is to quit the board affirms the change. (The position of Sir Win Bischoff, the banks chairman, is also reportedly under discussion; Mr Pandit looks more secure, if only because no one wants his job.) Not super at all

Universal banking need not fail. But smaller, focused organisations are easier to run than large, sprawling onesCitigroup has more employees than the American navy and, apparently, greater destructive power. Mr Weills creation, backed by a host of executives, directors and investors ever since, has proved horribly flawed. Unlike HSBC, another giant, Citi has been built through deal making and it shows. Acquisitions were poorly integrated. Cultures overlapped rather than melded (the resilience of the Smith Barney name is one telling indicator). Risk management was dismal. The big balance-sheet was deployed recklessly. It may be inevitable that some banks are too big to fail; but the lesson of Citi is that they can also be too big to manage.

The second shift in thinking signalled by Citis manoeuvres concerns policy. Novembers dramatic government intervention may have quelled fears that the bank would go under. But it has not stopped the bleeding at Citi, which remains focused on survival rather than on ramping up credit. Red ink laps around a host of other banks too. Full-year earnings at American banks are likely to be awful. Many eyes are on Bank of America, whose levels of tangible equity are also thin and, with Merrill Lynch and Countrywide to digest, is seeking billions of dollars in additional capital from the government. In Europe Deutsche Bank revealed a fourth-quarter loss of 4.8 billion ($6.3 billion) on January 14th, thanks in part to misplaced trading bets.

Recognition is growing that bad assets must somehow be purged from banks balance-sheets before they will freely make new loans. Citi has already had more than $300 billion of toxic assets ringfenced and guaranteed by the government; its apparent intention to create a separate entity for its unwanted assets is a more straightforward echo of the good bank/bad bank approach used in Swedens much-vaunted bail-out of the 1990s. In a speech on January 13th Ben Bernanke, chairman of the Federal Reserve, pointedly highlighted the continuing need for the financial system to shed its toxic assets.

That was the original purpose of the $700 billion Troubled Asset Relief Programme (TARP), approved in October, an effort that largely foundered on the difficulties of setting a purchase price for bad assets. The valuation problem has not gone away. Given the further deterioration in markets since the autumn, few believe that the $350 billion still left to spend from the TARP, if Congress agrees to release it, is anywhere near enough to absorb all the poison in the system. Even so, Citis shift in direction may signal that policymakers are looking again at the idea of bad banks. After all, one U-turn deserves another.

Author

Author

Logged

Logged

pardise.jpg

pardise.jpg

... good thing my high testosterone level has rendered me mostly hairless.

... good thing my high testosterone level has rendered me mostly hairless.